Entity Clarity Report — Energy in the AI Era: Q2 2026 Update

Summary

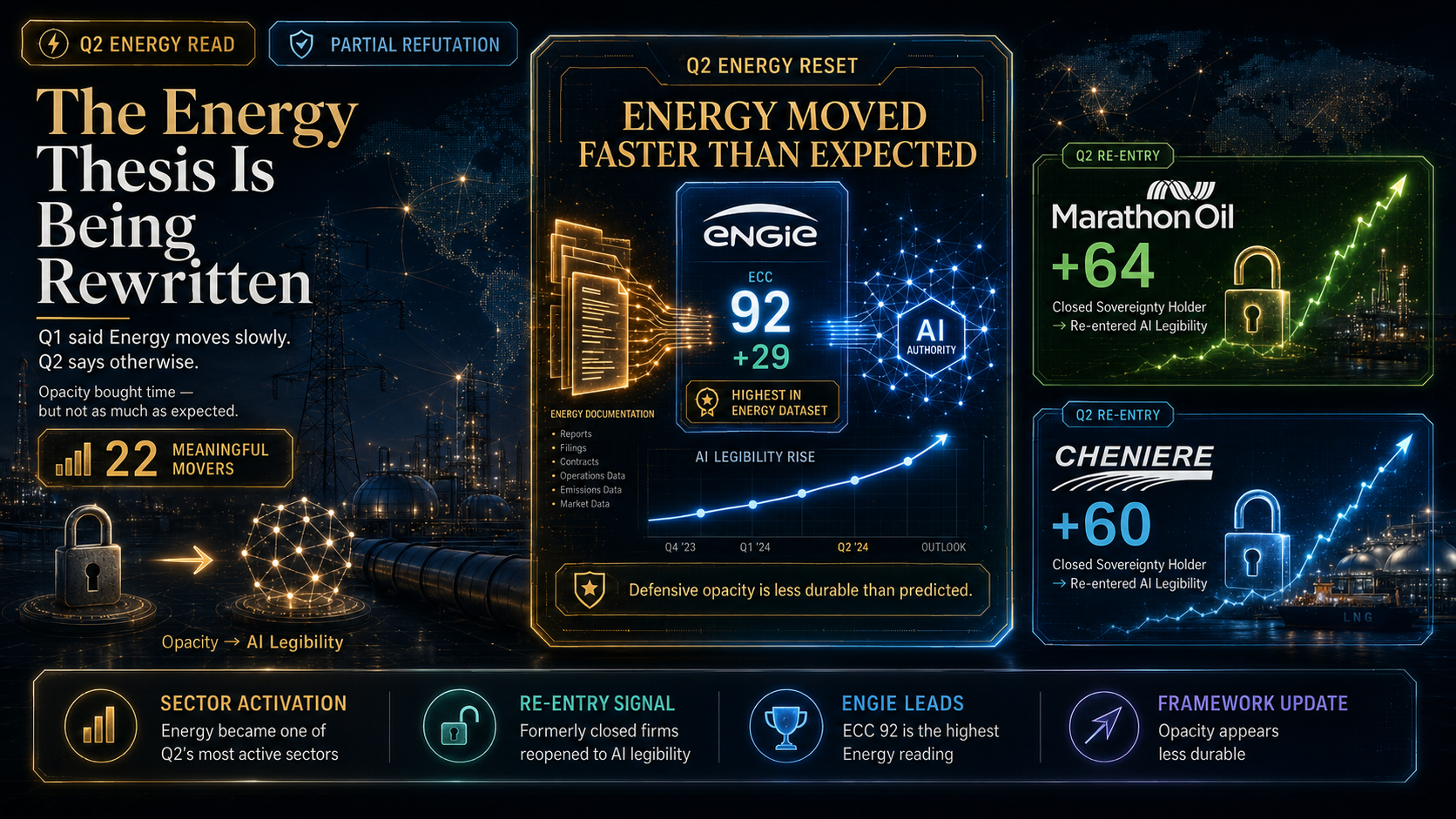

The Q1 Energy thesis — that the sector moves slowly, defensive postures are temporary, and opacity is the rational choice for state-backed or geopolitically sensitive firms — is partially refuted by Q2. Energy is now one of the most active sectors in the Q2 dataset, with 22 meaningful movers. Two Q1 Closed Sovereignty Holders re-entered AI legibility (Marathon Oil +64, Cheniere +60). Engie's +29 leap takes it to ECC 92, the highest in the Energy dataset. The Q1 prediction that opacity buys time appears less durable than the framework originally suggested.

Methodology

No changes to the ECC framework were made for Q2.

Posture definitions, capability tiers, and the three weighted ECC components — Entity Comprehension & Trust, Structural Data Fidelity, and Page-Level Hygiene — remain as published in the Q1 report.

Two methodology notes specific to Q2 Energy:

One — The volume of movement in Q2 Energy (approximately 22 movers in a 50-company dataset, or 44%) is materially higher than the Q1 framework predicted. The Q1 report characterized Energy as a slow-moving sector where defensive postures represent temporary equilibria. Q2 demonstrates the temporary character of those equilibria is shorter than the framework anticipated — meaning movement is more frequent than the Q1 framing implied. This is a finding the framework should track explicitly in Q3.

Two — Several Q2 moves involve large ECC gains without posture or capability changes (Cenovus +54, Marathon Oil +64 with posture and capability change). Cenovus's move in particular parallels the Q1 Amazon eCommerce situation: a company starting at ECC 5 that demonstrated rapid structural improvement is possible within a single quarter when leadership commits to the underlying work.

The full Q2 index with company-by-company values is available in the Q1 baseline report. Twenty-two companies moved meaningfully; this update covers the largest moves directly and groups smaller drift movements.

See details on the 13-signal framework

Findings

Six findings emerge from the Q2 Energy reading.

1. Energy is moving faster than the Q1 framework predicted

The Q1 Energy report characterized the sector as one where strategic posture changes would occur at the pace of capital cycles, regulatory consultation periods, and geopolitical re-evaluation. The framework treated movement between archetypes as exceptional rather than routine.

Q2 records 22 meaningful movers in a 50-company dataset — a 44% movement rate. By comparison, Q2 Tech recorded 17% movement, Q2 Finance recorded 14% movement, Q2 Payments recorded 19% movement, and Q2 Consulting recorded 20% movement. Only Media moved more (33%).

The framework should not have expected this. The Q1 thesis assumed energy firms would move slowly because their core stakeholders (institutional capital, regulators, sovereign governments) themselves move slowly. Q2 indicates either that the Q1 thesis was wrong about pace, or that the inflection point at which AI-mediated discovery affects capital allocation has accelerated.

The strategic implication: energy executives who treated AI legibility as a slow-moving optional investment in Q1 are now competing against peers who treated it as an urgent strategic decision in Q2. The gap between fast and slow movers in this sector is widening more rapidly than in any other quarterly reading.

2. The Closed Sovereignty Holders archetype is more permeable than the Q1 framework predicted

Marathon Oil moved from Blocked/Low/0 to Open/Medium/64 — a +64 ECC gain with both posture and capability changes. Cheniere Energy moved from Blocked/Low/0 to Defensive/Medium/60 — a +60 gain with both posture and capability changes.

Both companies were specifically listed in the Q1 Closed Sovereignty Holders archetype. The Q1 framework framed this archetype as a stable strategic position for "state-backed, asset-sovereign, or geopolitically sensitive firms" — implying durability and rational opacity. Q2 indicates the archetype is more permeable than that framing suggested.

The pattern is now cross-sector. Marathon Oil's +64 and Cheniere's +60 are structurally identical to Al Jazeera's +66 (Media Q2), Marsh & McLennan's +65 (Finance Q2), eBay's +60 (eCommerce Q2). Across all four sectors, Q1 Closed-archetype members re-entered AI legibility at remarkably consistent magnitudes (+60 to +66 ECC). The strategic logic is the same in each case: the institution concluded that the cost of being unread now exceeds the value of the control that Blocked posture provided.

For the remaining Q1 Closed Sovereignty Holders in energy (Chevron, PetroChina, Iberdrola, Duke Energy, Occidental Petroleum, Diamondback Energy, Marathon Petroleum), the Q2 evidence raises a strategic question: their Blocked positions are no longer mirror images of each other. Some peers have reversed course. The decision to remain Blocked is now an active choice that requires justification each quarter, rather than a default.

Watch Q3 for additional Closed Sovereignty Holder reversals. The Marathon Oil and Cheniere moves established that the path is operationally viable. Other Blocked energy firms now have a precedent to consider.

3. The Engie leap demonstrates that European energy firms can lead Authority Compounder positioning

Engie moved from Open/Medium/63 to Open/High/92 — a +29 ECC gain with capability moving from Medium to High. Engie is now the highest-scored entity in the Q2 Energy dataset.

This is the second-largest pure ECC move in the Q2 Energy reading (behind Cenovus's +54 at constant capability tier), and the largest move that includes a capability tier upgrade. Engie is also the first European energy firm to reach the top of the Energy ECC dataset — a position that in Q1 was held by US infrastructure companies (Williams Companies at 84, Phillips 66 at 84) and Saudi Aramco (75).

The strategic interpretation is sector-specific. Engie operates at the intersection of EU climate regulation, renewable energy deployment, and traditional utility infrastructure. Each of these business lines benefits from AI-legibility — EU regulators use AI tools to assess transition compliance, ESG capital allocators use AI to compare renewables positioning, and traditional utility customers use AI to navigate energy choice. By moving to High capability with ECC 92, Engie has positioned itself as the default AI-readable answer when capital, regulators, or customers ask about European energy transition.

The Q3 question for Engie is whether the +29 gain holds and compounds, or whether it represents a one-time investment outcome. For other European energy firms (TotalEnergies, BP, Shell, Iberdrola, RWE, Enel), Engie's Q2 leap establishes a new reference point in the sector. The relative ranking of European energy firms for AI-mediated discovery has measurably shifted in one quarter.

4. The Cenovus +54 confirms the Amazon eCommerce pattern at sector level

Cenovus Energy moved from Open/Low/5 to Open/Low/59 — a +54 ECC gain without changing posture or capability tier. The move parallels Amazon's Q1 → Q2 eCommerce trajectory exactly: a company starting at ECC 5 that demonstrated rapid structural improvement within a single quarter.

Cenovus did not cross the threshold into Medium capability tier in Q2, meaning the +54 gain occurred entirely within the Low capability band. This is significant because it indicates the firm did substantial documentation, schema, and entity work that produced large ECC gains before the cumulative effect was large enough to move tiers. The Q3 reading will likely show Cenovus crossing into Medium capability if the trajectory continues.

The cross-sector pattern (Amazon eComm +59, Cenovus Energy +54, Marathon Oil Energy +64, Visa Payments +9, Bloomberg Media -68 reversal) is establishing that single-quarter ECC reversals of meaningful magnitude (>±50 ECC points) are possible across multiple sectors when corporate leadership commits to the underlying work. The Q1 framework treated such moves as exceptional. Q2 indicates they are common enough to warrant routine analytical treatment.

5. The oilfield services and exploration tier is bifurcating

SLB (formerly Schlumberger) moved from Defensive/Medium/68 to Defensive/High/80 — a +12 ECC gain with capability moving from Medium to High. SLB is now the first oilfield services firm to enter Authority Compounder status while remaining in Defensive posture.

Equinor moved from Open/Medium/73 to Open/High/80 — a +7 gain with capability moving to High. Petrobras moved from Open/Medium/78 to Open/High/80 — a +2 ECC gain but with capability moving to High. Both companies are now Authority Compounders. The two firms join SLB as the three new High-capability entries in Q2.

The pattern is structurally meaningful. Non-US national or quasi-national oil firms (Equinor for Norway, Petrobras for Brazil) and global oilfield services firms (SLB) are moving up in Q2 while US shale and exploration firms drift down (Coterra -7, EOG holding at 35, Devon holding at 55, Imperial Oil capability dropping Medium → Low). The Q1 framework grouped these together as Open Legibility Builders. Q2 indicates the archetype is bifurcating into international upgraders (Equinor, Petrobras, SLB) and US-focused holders or driftors (Coterra, EOG, Devon, Imperial Oil).

The strategic implication is that AI-mediated capital allocation may be increasingly favoring non-US integrated and national oil firms over US shale-focused independents. The Q3 reading will indicate whether this geographic pattern continues or reverses.

6. The utilities tier is showing mixed signals

Constellation Energy moved from Open/High/81 to Open/Medium/74 — a -7 ECC drop with capability moving from High to Medium. NextEra Energy moved from Open/Medium/67 to Open/Medium/60 — a -7 drift at constant capability. Both are major US utilities.

Meanwhile, RWE held at Open/High/80 and PPL Corporation held at Open/High/80, both retaining Authority Compounder status. Southern Company moved +4 to ECC 72 (Medium capability held). National Grid moved +6 to ECC 69 (Medium capability held).

The pattern is mixed. Two large US utilities lost ground in Q2 while smaller US utilities drifted modestly upward and European utilities held position. The Q1 framework did not predict utility-tier bifurcation, and Q2 does not yet provide enough evidence to characterize the pattern definitively. The Q3 reading will indicate whether Constellation and NextEra recover, hold, or continue drifting — and whether the utility tier consolidates into a clear leadership group.

The Constellation -7 with capability loss is the most strategically important utility move because it crosses a tier threshold. Constellation was a Q1 Authority Compounder example specifically named in the report. Its Q2 move out of High capability is meaningful in the same way Citigroup's Q2 capability loss in Finance was meaningful: a Q1 archetype anchor lost its anchoring position.

Landscape

The Q1 Energy report framed the sector as one where AI legibility is a tool of capital and regulatory narrative management rather than consumer discovery. The Q1 framework predicted that opacity was a more rational posture for energy firms than for retailers, and that defensive postures represented temporary equilibria that would eventually resolve in either direction.

Q2 partially refutes that framing.

Energy is one of the most active sectors in the Q2 dataset. Approximately 22 companies in a 50-company set showed meaningful movement — a 44% movement rate, second only to Media's 33%. The Q1 framework treated Energy as slow-moving by structural necessity. Q2 demonstrates that when firms in the sector choose to invest in AI legibility, they can move ECC tiers within a single quarter.

Two Q1 Closed Sovereignty Holders re-entered AI legibility. Marathon Oil moved from Blocked/Low/0 to Open/Medium/64 (+64). Cheniere Energy moved from Blocked/Low/0 to Defensive/Medium/60 (+60). Both were specifically named in the Q1 Closed Sovereignty Holders archetype. Their Q2 re-entries parallel similar moves in Media (Al Jazeera +66), Finance (Marsh & McLennan +65), and eCommerce (eBay +60). Across four sectors now, Q1 Blocked or Closed-archetype members are choosing to re-enter AI legibility in Q2 at remarkably similar magnitudes (+60 to +66 ECC).

The pattern is now too consistent to be coincidental. The Q1 framework predicted Closed posture would be durable for sovereign and asset-protective reasons. Q2 indicates Closed posture is more frequently a strategic choice that gets re-evaluated than the Q1 framework suggested — and that the cost of being unread relative to AI-mediated capital and recommendation flows has crossed an inflection point for many institutions.

Engie's leap to ECC 92 is the largest positive ECC move in the Q2 Energy reading. Engie moved from Open/Medium/63 to Open/High/92 — a +29 gain with capability moving from Medium to High. Engie is now the highest-scored entity in the Q2 Energy dataset, ahead of every US oil major, every US utility, and every other European energy firm.

The strategic interpretation: a European integrated energy and utility firm with significant renewables exposure has positioned itself as the most AI-legible energy entity in the world within one quarter. This is structurally meaningful for European energy firms navigating both EU regulatory frameworks and ESG capital allocation pressures.

Cenovus's +54 is the quietest important move. Cenovus moved from Open/Low/5 to Open/Low/59 — a +54 ECC gain without changing posture or capability tier. This parallels the Q1 → Q2 Amazon trajectory in eCommerce: a company starting at ECC 5 (functionally invisible) demonstrating that rapid structural improvement is achievable within a single quarter. Capability tier did not change because Cenovus did not yet cross the threshold into Medium — but the underlying ECC gain is large enough that Cenovus is now reading as a mid-tier energy firm rather than a near-invisible one.

The Q1 thesis on Energy AI posture is intact in its broad strokes — the sector competes for AI-mediated judgment rather than consumer discovery, firms cluster into three archetypes (Open Legibility Builders, Defensive Narrative Managers, Closed Sovereignty Holders) — but the framework needs to revise its prediction about the durability of opacity and the speed of strategic decision-making within the sector.

Archetypes

The three archetypes from Q1 remain the framework. Q2 changes membership meaningfully in all three.

Open Legibility Builders (Open posture, structurally clear, ECC 70+)

New entries in Q2: Engie (now 92, +29, the new dataset leader), Petrobras (now 80, capability moved to High), Equinor (now 80, capability moved to High), Marathon Oil (now 64, formerly Closed Sovereignty Holder).

Lost from archetype: Constellation Energy (now Open/Medium/74, lost High capability).

Held position with drift: Williams Companies (84 → 91, +7), Phillips 66 (84 → 90, +6), ConocoPhillips (81 → 84, +3), Saudi Aramco (75 → 77, +2), APA Corporation (82 → 83, +1), RWE (held at 80), PPL Corporation (held at 80), Hess (held at 74).

Net direction: Significantly expanded. The archetype gained four members and lost one. The new entries include the first European energy firm to lead the dataset (Engie), the first two non-US national or quasi-national oil firms to reach Authority Compounder status (Petrobras, Equinor), and the first Closed-archetype-to-Open-archetype reversal in the sector (Marathon Oil).

The archetype is now the most diverse it has been in the Energy dataset by geography, business model, and ownership structure.

Defensive Narrative Managers (Defensive posture, controlled exposure)

New entry in Q2: Cheniere Energy (Blocked → Defensive, ECC 0 → 60), SLB (capability moved to High while remaining Defensive — now an Authority Compounder despite Defensive posture).

Held position with drift: BP (69 → 67, -2), Enel (held at 66), Reliance (held at 69), Baker Hughes (82 → 83, +1), Woodside (held at 78), GE Vernova (held at 63), Shell (held at 13).

Net direction: Mixed. Cheniere's entry represents an exit from the Closed Sovereignty Holders. SLB's capability move makes it the first Defensive-posture firm with High capability in the Energy dataset — a hybrid position the Q1 framework did not specifically anticipate.

The archetype's strategic positioning is becoming more nuanced. Defensive posture no longer implies Medium capability ceiling — SLB and Baker Hughes both now hold High capability while in Defensive posture. The "Defensive ceiling" the Q1 framework predicted may be lifting for oilfield services specifically, while remaining intact for integrated majors.

Closed Sovereignty Holders (Blocked posture, ECC 0)

Lost in Q2: Marathon Oil (to Open Legibility Builders), Cheniere Energy (to Defensive Narrative Managers).

Held position: Chevron, PetroChina, Iberdrola, Duke Energy, Occidental Petroleum, Diamondback Energy, Marathon Petroleum.

Net direction: Shrinking. The archetype lost two members and gained none. This is consistent with the cross-sector pattern of Closed-archetype erosion (Al Jazeera in Media, Marsh & McLennan in Finance, eBay in eCommerce, and now Marathon Oil and Cheniere in Energy).

The remaining members are a mix of US oil majors (Chevron, Occidental, Marathon Petroleum, Diamondback), state-backed firms (PetroChina), and utility companies (Iberdrola, Duke Energy). The strategic motivations across this group are not uniform. Chevron's Blocked posture is likely competitive and ESG-defensive. PetroChina's is sovereign and geopolitical. Iberdrola's and Duke Energy's are likely regulatory and customer-protective.

The Q3 question is whether any of these subgroups follows Marathon Oil's path. The most likely candidates for Q3 reversal are the US oil majors that face the most direct AI-mediated capital allocation pressure (Chevron in particular, given its size and shareholder base).

Index

Strategic Implications

Q1 Energy framed the sector as one where AI legibility serves capital and regulatory narrative management. Q2 sharpens that framing in four ways.

The "opacity buys time" thesis requires partial revision. The Q1 framework concluded with the line "opacity buys time — not immunity." Q2 demonstrates the time horizon is shorter than the framework implied. Two Closed Sovereignty Holders re-entered AI legibility in Q2 — within one quarter of being labeled as durably opaque. The remaining Closed members now face a choice that the Q1 framework did not require them to face explicitly: their Blocked positions are no longer mirror images of each other, and each quarter that they remain Blocked while peers move toward Open or Defensive postures represents accumulating relative disadvantage.

The international/US bifurcation is real and should be tracked. Engie at ECC 92, Petrobras and Equinor both upgrading to High capability, and SLB upgrading to High capability all occurred in Q2 — while major US utilities (Constellation, NextEra) drifted negatively, and US exploration firms (Coterra, Devon, Imperial Oil) held position or lost ground. This is the clearest geographic pattern in any Q2 ECC reading. The strategic interpretation is that AI-mediated capital allocation is currently favoring non-US integrated firms, European utilities with renewables exposure, and global oilfield services over US shale-focused independents. Whether this is a one-quarter pattern or a multi-quarter trend will be visible in Q3.

Defensive posture no longer caps capability at Medium. The Q1 framework predicted "ECC ceiling, risk of being framed as evasive" as the primary weakness of Defensive Narrative Managers. SLB's Q2 move to High capability while remaining Defensive (and Baker Hughes' continued High capability in Defensive posture) demonstrates this ceiling is more porous than the Q1 framework suggested for certain business model types. Oilfield services firms appear to be able to maintain Defensive posture and High capability simultaneously — possibly because their primary stakeholders (energy operators, regulators, equipment customers) value technical documentation specifically and respond well to controlled narrative exposure with strong structural fidelity.

This finding has implications beyond Energy. If Defensive posture can support High capability in oilfield services, the framework may need to revise its general predictions about Defensive posture ceilings across other sectors.

The pace of strategic decision-making in Energy is faster than the Q1 framework expected. The 44% Q2 movement rate is materially higher than the Q1 thesis predicted. Energy executives who treated AI legibility as a slow-moving optional investment in Q1 are now competing against peers who treated it as an urgent strategic decision in Q2. The gap between fast and slow movers in Energy is widening more rapidly than in any other sector covered in the Q2 cycle.

The Q3 question for Energy is whether the Q2 movement was a one-quarter catch-up effect (a wave of firms responding simultaneously to capital and regulatory pressure that had been accumulating since Q1) or the beginning of a sustained pattern of faster decision-making in the sector. If Q3 shows similar movement volumes, the framework should formally revise its slow-sector characterization of Energy.

Full Report

Energy's AI thesis in Q1 was that the sector moves slowly, defensively, and rationally toward opacity when the firm's stakeholders are sovereign, institutional, or geopolitically sensitive. Q2 partially refutes all three of those claims.

The sector is moving faster than predicted. Energy recorded approximately 22 meaningful movers in a 50-company dataset — a 44% movement rate, second only to Media's 33% across the six Q2 sector readings. The Q1 framework treated Energy as one of the slower-moving sectors in the dataset by structural necessity (capital cycle pace, regulatory consultation periods, geopolitical inertia). Q2 demonstrates that when energy firms choose to invest in AI legibility, they can move tiers within a single quarter — and that approximately half the sector has now done so.

The strategic implication is that Q1 was the calm before a sector-wide repositioning. Energy executives who treated AI legibility as a slow optional investment in Q1 are now competing against peers who treated it as urgent. The Q1 → Q2 gap between fast and slow movers in Energy is now wider than in any other sector covered in the Q2 cycle.

Two Closed Sovereignty Holders re-entered AI legibility in Q2. Marathon Oil moved from Blocked/Low/0 to Open/Medium/64 — a +64 ECC gain with both posture and capability changes. Cheniere Energy moved from Blocked/Low/0 to Defensive/Medium/60 — a +60 ECC gain with both posture and capability changes. Both companies were specifically named in the Q1 Closed Sovereignty Holders archetype.

The cross-sector pattern is now too consistent to be coincidental. Marathon Oil +64 (Energy Q2), Cheniere +60 (Energy Q2), Al Jazeera +66 (Media Q2), Marsh & McLennan +65 (Finance Q2), eBay +60 (eCommerce Q2). Across four sectors, Q1 Closed-archetype members are reversing course in Q2 at remarkably similar magnitudes (+60 to +66 ECC). The Q1 framework predicted Closed posture would be durable for sovereign, asset-protective, and competitive reasons. Q2 indicates Closed posture is more frequently a strategic choice that gets actively re-evaluated than the Q1 framework anticipated.

The strategic logic across these cases is identical: the institution concluded that the cost of being unread by AI systems now exceeds the value of the control that Blocked posture provides. This is the most important framework-level finding of the Q2 cycle — Blocked posture has become a higher-cost choice in Q2 than it was in Q1, and the institutions making different decisions about that cost are visible in the data.

For the remaining Q1 Energy Closed Sovereignty Holders (Chevron, PetroChina, Iberdrola, Duke Energy, Occidental Petroleum, Diamondback Energy, Marathon Petroleum), the Q2 evidence raises a strategic question that the Q1 framework did not require them to address. Their Blocked positions are no longer mirror images of each other. Each quarter that they remain Blocked while peers reverse course represents accumulating relative disadvantage in AI-mediated capital allocation, regulatory framing, and stakeholder discovery.

Engie's leap to ECC 92 is the largest tier-changing positive move in Q2 Energy. Engie moved from Open/Medium/63 to Open/High/92 — a +29 ECC gain with capability moving from Medium to High. Engie is now the highest-scored entity in the Q2 Energy dataset, ahead of every US oil major, every US utility, and every other European energy firm.

The strategic interpretation is sector-specific and important. Engie operates at the intersection of EU climate regulation, renewable energy deployment, and traditional utility infrastructure — each of which has substantial AI-mediated stakeholder exposure. EU regulators increasingly use AI tools to assess transition compliance. ESG capital allocators use AI to compare renewables positioning. Customers use AI to navigate energy choice. By moving to ECC 92 with High capability, Engie has positioned itself as the default AI-readable answer when any of these stakeholders asks about European energy transition.

The competitive implication for European energy firms is direct. TotalEnergies, BP, Shell, Iberdrola, RWE, and Enel now have a clear reference point in the sector that they did not have in Q1. The relative AI-mediated ranking of European energy firms has measurably shifted in one quarter, and Engie is now the leader by a substantial margin (92 vs. the next-closest European Authority Compounder at 80).

The Cenovus +54 is the quietest important move. Cenovus Energy moved from Open/Low/5 to Open/Low/59 — a +54 ECC gain without changing posture or capability tier. The trajectory parallels Amazon's Q1 → Q2 eCommerce trajectory: a company starting at ECC 5 demonstrating rapid structural improvement within a single quarter. Cenovus's gain occurred entirely within the Low capability band, meaning the underlying documentation and entity work was substantial but not yet enough to push the firm into the next tier.

This kind of move — large ECC gain within a single tier — is increasingly common across the Q2 cycle. The framework's Q3 methodology may benefit from a formal indicator for "within-tier acceleration" that captures structural progress before it crystallizes into a tier change. Without such an indicator, firms doing serious documentation work but not yet crossing tier thresholds are obscured in the data.

The international/US bifurcation is the strongest geographic signal in any Q2 reading. SLB upgraded to High capability while remaining Defensive (now Authority Compounder despite Defensive posture). Equinor (Norway) and Petrobras (Brazil) both upgraded from Medium to High capability and are now Authority Compounders. Engie (France) made its +29 move. Meanwhile, Constellation Energy (US) lost High capability, NextEra (US) drifted -7, Coterra (US) drifted -7, Imperial Oil capability dropped Medium → Low.

The pattern is clear: non-US integrated firms, European utilities with renewables exposure, and global oilfield services are moving up; US utilities and US shale-focused independents are drifting down. The Q1 framework grouped these together as Open Legibility Builders. Q2 indicates the archetype is bifurcating along geographic and business model lines.

The strategic implication is that AI-mediated capital allocation is currently favoring international firms over US-focused independents within the energy sector. This is the clearest sector-level geographic shift in any Q2 reading. Whether this is a one-quarter pattern reflecting deferred Q1 decisions or the beginning of a multi-quarter trend will be visible in Q3.

Defensive posture no longer caps capability at Medium for oilfield services. SLB's move to High capability while remaining in Defensive posture is structurally novel. The Q1 framework predicted "ECC ceiling" as the primary weakness of Defensive Narrative Managers — implying that Defensive posture inherently limits capability development. SLB's Q2 move (and Baker Hughes' continued High capability in Defensive posture) demonstrates this ceiling is permeable for certain business model types.

The strategic interpretation is that oilfield services firms appear able to maintain Defensive posture and High capability simultaneously because their primary stakeholders (energy operators, regulators, equipment customers) value technical documentation specifically. Defensive posture preserves competitive intelligence and regulatory optionality while still allowing for strong structural disclosure of capability, technology, and reliability claims. This is a hybrid position the Q1 framework did not anticipate, and it may apply to other technical service industries beyond energy.

The utilities tier is showing mixed signals that warrant Q3 monitoring. Constellation Energy's -7 with High → Medium capability is the most strategically important utility move because it crosses a tier threshold. Constellation was a Q1 Authority Compounder named specifically in the framework. Its Q2 capability loss is meaningful in the same way Citigroup's Q2 capability loss in Finance was meaningful: a Q1 archetype anchor lost its anchoring position. NextEra's -7 drift adds a second large US utility moving downward.

Meanwhile, RWE and PPL held High capability, Southern Company drifted +4, and National Grid drifted +6. The utility tier is not collapsing, but it is clearly not consolidating around US utility leadership. European and selectively-positioned US utilities are holding. The largest US-focused utilities are drifting.

Seven questions will frame the Q3 reading on Energy:

- Does Marathon Oil and Cheniere's re-entry hold? If Q3 shows further gains or stability, the Closed Sovereignty Holders archetype will need formal redefinition.

- Do additional Closed Sovereignty Holders follow? Chevron in particular faces the most direct AI-mediated capital pressure given its size and shareholder base.

- Does Engie's +29 leap to ECC 92 hold or compound? If Engie remains at the top of the dataset through Q3, the European energy leadership position is durable.

- Does the international/US bifurcation continue? If Petrobras, Equinor, SLB, and Engie hold while US utilities and exploration firms continue drifting, the framework will need to formally track geography as a Q3 dimension.

- Does Cenovus cross into Medium capability tier? The +54 trajectory predicts yes; if so, the framework's "within-tier acceleration" indicator becomes important.

- Does SLB's High capability with Defensive posture hold? This combination challenges the Q1 framework's capability-posture coupling and may need to be tracked as a distinct hybrid archetype.

- Do Constellation Energy and NextEra recover, or continue drifting? Utility-tier leadership in the US is the most open competitive question in the sector.

The Q1 Energy thesis is partially intact and partially refuted. Energy still competes for AI-mediated judgment rather than consumer discovery. Energy firms still cluster into Open, Defensive, and Closed archetypes. What Q2 changes is the pace of strategic decision-making in the sector, the durability of Closed positions, the capability ceiling of Defensive postures, and the geographic distribution of Authority Compounder status. The sector is moving faster, the archetypes are more permeable, and the leadership is more international than the Q1 framework predicted.

This is the largest quarterly correction to the framework's predictions in any Q2 reading. Energy was supposed to be slow. It isn't.