Entity Clarity Report — Payments & Financial Infrastructure: Q2 2026 Update

Summary

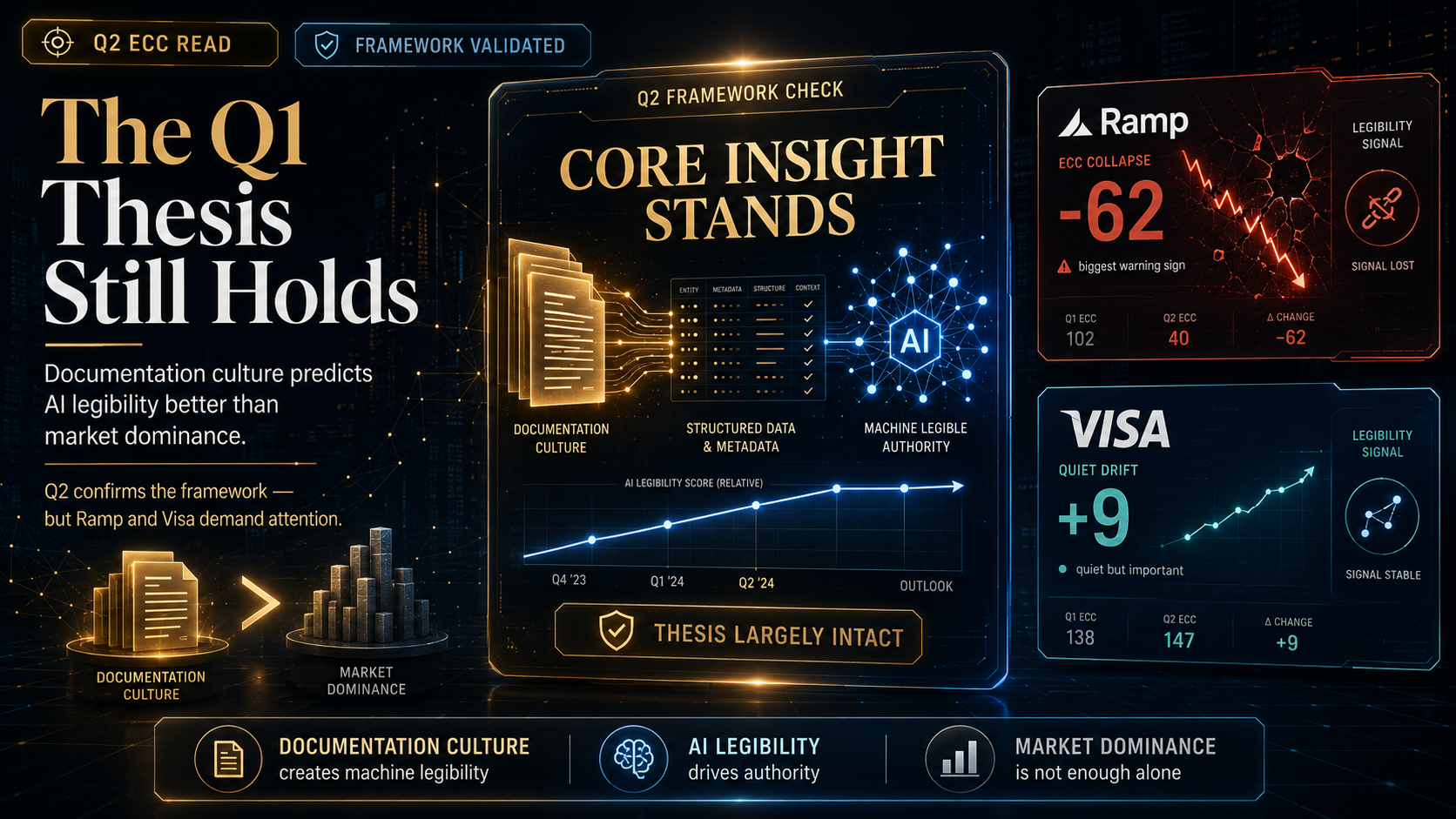

The Q1 thesis — that documentation culture predicts AI legibility better than market dominance — is largely intact in Q2. Nine companies moved, with most movement reinforcing the original archetype assignments. Two findings demand attention: Ramp's -62 ECC collapse from Authority Compounder to Open but Unresolved (the largest negative ECC move in any Q2 reading), and Visa's quiet +9 drift that suggests the network paradox is partially beginning to close. The crypto Authority Compounders (Circle, Fireblocks) drifted negatively. The cross-border money-movement cluster (dLocal, Flywire, Green Dot) drifted positively. The Q1 framework's core insight stands.

Methodology

No changes to the ECC framework were made for Q2.

Posture definitions, capability tiers, and the three weighted ECC components — Entity Comprehension & Trust, Structural Data Fidelity, and Page-Level Hygiene — remain as published in the Q1 report.

Two methodology notes specific to Q2 Payments:

One — The framework cannot directly observe what causes large ECC moves between quarters. Ramp's -62 ECC drop, in particular, requires direct explanation that the framework can document but not generate: the change is consistent with a major site restructuring, schema breakage, or deliberate documentation revision. Whether this is a temporary artifact or a structural reversal will be visible in Q3.

Two — American Express appears in this dataset and the Finance dataset with different Q1 and Q2 trajectories. In Payments, AmEx held at Open/Medium/68. In Finance, AmEx moved from Defensive to Open at the same ECC. This is the second case of the same parent entity appearing in two ECC reports with divergent operational trajectories (Marsh McLennan being the first), supporting the conglomerate disaggregation pattern emerging across the Q2 dataset.

The full Q2 index with company-by-company values is available in the Q1 baseline report. Only nine companies moved meaningfully; this update covers them directly.

See details on the 13-signal framework

Field 8: Landscape Overview (Rich text)

The Q1 Payments report identified a structural truth: documentation culture predicts AI legibility better than market dominance. The Q1 framework recorded developer-first companies (Stripe, Adyen, Fireblocks, Checkout.com) at exceptional clarity while the largest payments rails (Visa, Mastercard) were either blocked or unresolved. The signature finding was the network paradox: Stripe was nearly twice as legible to AI systems as Visa, despite Visa processing 15× the transaction volume.

Q2 leaves that finding largely intact, with two refinements.

The network paradox is beginning to soften. Visa moved from ECC 43 to ECC 52 — a +9 drift without posture or capability change. The shift is small in absolute terms but meaningful in context: Visa is the largest payments network by volume, and any movement in its ECC reading indicates documentation work that simply was not happening in Q1. The Q1 framework framed Visa as the marquee example of "open but unresolved." The Q2 reading shows Visa beginning to address that — though not enough to leave the archetype.

Mastercard remains at 0. Global Payments, Worldline, and Toast remain at 0. The four Q1 Closed Holders in payments held their positions. Visa's movement is structurally isolated within the network tier.

The Ramp collapse is the largest negative move in any Q2 reading. Ramp moved from Open/High/80 to Open/Low/18 — a -62 ECC drop with capability falling two tiers from High to Low. Ramp was specifically named in the Q1 report as one of the developer-first private fintechs that anchored the documentation-culture thesis. A -62 collapse from one of the Q1 thesis exemplars is consequential.

The strategic interpretation matters more than the numerical drop. The Q1 framework treated Authority Compounder status as the product of sustained documentation discipline. Ramp's Q2 reading suggests Authority Compounder status is operationally fragile: a single major site change, schema migration, or content restructuring can erase the structural infrastructure that produced the original High capability rating. The framework needs to track whether this is a one-quarter event or the beginning of a sustained reversal.

The remaining seven movers either confirm or extend the Q1 documentation-culture thesis. dLocal moved from Medium to High capability (ECC 67 → 90, +23) — now an Authority Compounder. Green Dot moved from Medium to High capability (ECC 69 → 86, +17) — also now an Authority Compounder. Flywire moved Medium → High (ECC 73 → 81, +8). Nexi gained +7. Nuvei flipped Defensive to Open with +9 ECC. Circle and Fireblocks drifted negatively (-10 and -6). Affirm drifted -7.

The pattern is structurally coherent: the firms doing documentation work moved up. The firms that were the strongest exemplars of documentation culture (Circle, Fireblocks, Ramp) drifted down. The middle of the dataset held position.

Findings

Five findings emerge from the Q2 Payments reading.

1. The Ramp collapse is the largest negative ECC move in any Q2 reading and the most strategically consequential

Ramp moved from Open/High/80 to Open/Low/18 — a -62 ECC drop. Capability moved two tiers from High to Low. Posture held at Open.

This is the largest negative ECC move in any Q2 ECC reading across Tech, Media, Finance, Consulting, eCommerce, and Payments. It is larger than Sky News' Q2 Media exit (-86 included a posture move to Blocked, but here Ramp held Open and still lost two capability tiers). It is larger than Applied Materials' Q2 Tech exit (-91 included a posture move to Blocked). What makes Ramp's collapse strategically consequential is that posture remained constant — meaning the loss is purely structural rather than strategic.

The Q1 Payments report explicitly named Ramp as one of the seven developer-first private fintechs that anchored the documentation-culture thesis. The other six (Stripe, Checkout.com, Fireblocks, Rapyd, Plaid, Brex) all held position or drifted modestly. Ramp's collapse is therefore an isolated structural event within a group that otherwise held together.

Three possible explanations:

One — A major site restructuring, rebranding, or platform migration broke the structural infrastructure that supported the Q1 ECC 80. This is the most common cause of large ECC capability drops at constant posture.

Two — A deliberate documentation revision that prioritized a different audience (institutional customers vs. developers, for example) and inadvertently reduced AI-legibility as a byproduct.

Three — A measurement artifact where the Q1 reading captured a temporary peak state that has since normalized.

The Q3 reading will distinguish among these. If Ramp recovers to ECC 60+ in Q3, the Q2 reading was an event tied to a discrete transition. If Ramp stays at ECC 18, the Q2 reading captured a structural decision. If Ramp returns to the 80s, Q1 was the anomaly.

For other Authority Compounders in the dataset, the implication is that the Q1 framework's central thesis is operationally vulnerable. Documentation discipline produces AI legibility — and any disruption to that discipline can erase the legibility quickly.

2. Visa's +9 drift signals the network paradox is partially closing

Visa moved from ECC 43 to ECC 52 — a +9 drift, no posture change, no capability change. The Q1 framework identified Visa as the marquee example of "open but unresolved" — the network that processes 15× more transaction volume than any other payments entity but cannot be coherently explained by AI systems.

The Q2 +9 is small in isolation but structurally significant. Visa is the largest payments network in the world. Any movement in its ECC reading indicates documentation infrastructure work that simply was not happening in Q1. The trajectory matters more than the magnitude.

Two interpretations are possible:

One — Visa is beginning a multi-quarter ECC improvement trajectory similar to Amazon's Q2 eCommerce reversal, but at a slower pace because the underlying technical and regulatory complexity is larger.

Two — The +9 is a one-quarter drift that will not continue, leaving Visa in the Open but Unresolved archetype indefinitely.

The strategic question for Mastercard is sharper. Visa is open and slowly improving. Mastercard remains at ECC 0 — Blocked. If Visa continues its drift in Q3 and reaches ECC 60+ by Q4, Mastercard will face a clear competitive disadvantage in AI-mediated payments recommendation. The two networks have historically operated as a duopoly with rough strategic parity. Q2 introduces the first measurable structural divergence between them.

For other Q1 "Open but Unresolved" members (Block/Square 52, UnionPay 49, JCB 39, International Money Express 56), Visa's movement establishes that the archetype is not a permanent state. It can be exited through documentation work. The Q3 reading will indicate whether any of these firms follow Visa's path.

3. The dLocal and Green Dot promotions confirm the cross-border money-movement thesis

dLocal moved from Open/Medium/67 to Open/High/90 — a +23 ECC gain with capability moving from Medium to High. Green Dot moved from Open/Medium/69 to Open/High/86 — a +17 ECC gain with capability moving from Medium to High. Both companies now sit in the Authority Compounder archetype.

The Q1 framework's segment analysis showed Money Movement as the highest-ECC payments segment (average ECC 74.4, 57% High Capability). Q2 reinforces this finding: dLocal and Green Dot are the two largest positive movers in the dataset, and both are cross-border or alternative money-movement specialists.

The Q1 framework attributed money-movement outperformance to two factors: regulatory documentation requirements (which produce AI-legible compliance content as a byproduct) and developer-first API documentation (which money-movement firms invest in heavily to support fintech integrations). Q2's dLocal and Green Dot gains support both interpretations.

dLocal specifically — focused on emerging-market cross-border payments — is now ECC 90, the second-highest score in the Q2 Payments dataset behind only Fireblocks' 85 (which drifted down from 91). dLocal's ascent represents the first non-US/non-Western entity to reach top-tier Authority Compounder status in any Q2 ECC reading.

The implication: the network paradox is real, but it does not apply uniformly across all payments segments. Networks are invisible. Money-movement firms are highly visible. AI recommendation flows accordingly.

4. The crypto Authority Compounders drifted negatively

Circle moved from Open/High/83 to Open/Medium/73 — a -10 ECC drop with capability falling from High to Medium. Fireblocks moved from Open/High/91 to Open/High/85 — a -6 drift, capability held at High.

The Q1 framework identified crypto infrastructure as showing "extreme divergence" — Coinbase blocked at 0 while Circle and Fireblocks were among the clearest entities in the entire dataset. The Q1 explanation was that regulatory-clarity requirements for stablecoins produce AI-legibility as a byproduct.

Q2 introduces a question that did not exist in Q1: is the crypto AI-legibility advantage durable, or is it a transient state tied to a specific regulatory moment?

Circle's drop from 83 to 73 is structurally meaningful — losing the High capability tier suggests measurable structural changes to the firm's AI-legibility infrastructure. Fireblocks held High capability but lost ECC, suggesting smaller schema or content changes. Neither move is large in isolation, but both are negative within an archetype the Q1 framework specifically called out as exceptional.

If Q3 shows continued negative drift, the Q1 thesis on crypto-as-AI-legibility-leader will need partial revision. If Q3 shows recovery, the Q2 drift was tactical rather than structural.

5. Three middle-tier promotions confirm the Q1 documentation-culture thesis

Flywire moved from Open/Medium/73 to Open/High/81 (+8, Medium → High). Nexi moved from Open/Medium/69 to Open/Medium/76 (+7, capability held). Nuvei moved from Defensive/Medium/64 to Open/Medium/73 (+9, posture changed from Defensive to Open).

All three are payments infrastructure firms moving from middle-tier to upper-middle-tier ECC. None broke into Authority Compounder territory in Q2, but all three are now closer to that threshold. The pattern is consistent: deliberate documentation work produces measurable ECC gains within a single quarter.

The Nuvei posture shift specifically — Defensive to Open at +9 ECC — is the inverse of the Burlington Stores Q2 eCommerce move (Open to Defensive at constant ECC). Nuvei is the fifth cross-sector example of posture experimentation, but distinct from the previous four because the posture change accompanied an ECC gain. This may represent a different pattern: structural decision to open posture as a deliberate competitive move, rather than experimentation at constant capability.

If more firms make Nuvei-style structural posture changes (Defensive → Open with measurable ECC gain), the framework may need to distinguish:

- Experimental posture changes at constant ECC and capability (Burlington, AmEx, Nu Holdings, Publicis Sapient)

- Structural posture changes with accompanying ECC and capability gains (Nuvei)

These are different strategic decisions and likely produce different downstream outcomes.

Landscape

The Q1 Payments report identified a structural truth: documentation culture predicts AI legibility better than market dominance. The Q1 framework recorded developer-first companies (Stripe, Adyen, Fireblocks, Checkout.com) at exceptional clarity while the largest payments rails (Visa, Mastercard) were either blocked or unresolved. The signature finding was the network paradox: Stripe was nearly twice as legible to AI systems as Visa, despite Visa processing 15× the transaction volume.

Q2 leaves that finding largely intact, with two refinements.

The network paradox is beginning to soften. Visa moved from ECC 43 to ECC 52 — a +9 drift without posture or capability change. The shift is small in absolute terms but meaningful in context: Visa is the largest payments network by volume, and any movement in its ECC reading indicates documentation work that simply was not happening in Q1. The Q1 framework framed Visa as the marquee example of "open but unresolved." The Q2 reading shows Visa beginning to address that — though not enough to leave the archetype.

Mastercard remains at 0. Global Payments, Worldline, and Toast remain at 0. The four Q1 Closed Holders in payments held their positions. Visa's movement is structurally isolated within the network tier.

The Ramp collapse is the largest negative move in any Q2 reading. Ramp moved from Open/High/80 to Open/Low/18 — a -62 ECC drop with capability falling two tiers from High to Low. Ramp was specifically named in the Q1 report as one of the developer-first private fintechs that anchored the documentation-culture thesis. A -62 collapse from one of the Q1 thesis exemplars is consequential.

The strategic interpretation matters more than the numerical drop. The Q1 framework treated Authority Compounder status as the product of sustained documentation discipline. Ramp's Q2 reading suggests Authority Compounder status is operationally fragile: a single major site change, schema migration, or content restructuring can erase the structural infrastructure that produced the original High capability rating. The framework needs to track whether this is a one-quarter event or the beginning of a sustained reversal.

The remaining seven movers either confirm or extend the Q1 documentation-culture thesis. dLocal moved from Medium to High capability (ECC 67 → 90, +23) — now an Authority Compounder. Green Dot moved from Medium to High capability (ECC 69 → 86, +17) — also now an Authority Compounder. Flywire moved Medium → High (ECC 73 → 81, +8). Nexi gained +7. Nuvei flipped Defensive to Open with +9 ECC. Circle and Fireblocks drifted negatively (-10 and -6). Affirm drifted -7.

The pattern is structurally coherent: the firms doing documentation work moved up. The firms that were the strongest exemplars of documentation culture (Circle, Fireblocks, Ramp) drifted down. The middle of the dataset held position.

Archetypes

The five archetypes from Q1 remain the framework. Q2 changes membership meaningfully in three of them.

Authority Compounders (ECC ≥ 80, deliberate AI-legibility design)

Joined in Q2: dLocal (now 90), Green Dot (now 86), Flywire (now 81).

Lost in Q2: Ramp (now 18, Open but Unresolved), Circle (now 73, Infrastructure Legibility Builder).

Held position with drift: Fireblocks (91 → 85), Evertec (89), Paysafe (88), Payoneer (86), Remitly (85), Rapyd (85), WEX (84), Discover (83), SS&C (83), Stripe (82), Western Union (82), Adyen (81), Checkout.com (81), Marqeta (81), PagSeguro (81).

Net direction: Net positive composition change. Three new members entered (dLocal, Green Dot, Flywire). Two members exited (Ramp, Circle). The archetype is more populous than in Q1, but with composition that is now more geographically distributed (dLocal in Latin America joining the existing Latin American members PagSeguro and Evertec).

The Ramp exit is the strategically consequential change. The other moves within the archetype are either drift or composition rebalancing.

Infrastructure Legibility Builders (ECC 65-79)

Joined in Q2: Circle (from Authority Compounder), Nuvei (from Defensive Narrative Manager).

Lost in Q2: Flywire (now Authority Compounder), Nexi (still in archetype but moved up to ECC 76).

Held position with drift: Wise (78), Fiserv (76), Brex (73), Corpay (73), Plaid (70), Bill Holdings (69), American Express (68), Affirm (60 — drifted down).

Net direction: Stable composition with internal repositioning. The archetype gained one Authority Compounder downgrade (Circle) and one Defensive promotion (Nuvei), while losing two firms upward. The pattern is healthy: firms are moving in and out, but the size and structure of the archetype remain similar to Q1.

Defensive Narrative Managers (Defensive posture)

Lost in Q2: Nuvei (moved to Open).

Held position with no movement: Discover (83), WEX (84), Western Union (82), Adyen (81), Wise (78), MoneyGram (69), PayPal (64), Klarna (60), StoneCo (53).

Net direction: Stable. The Q1 thesis that Defensive posture in payments preserves flexibility while maintaining visibility appears to hold. No firm in this archetype made large moves in Q2.

Open but Unresolved (Open posture, ECC < 60, large operational footprint)

Held position: Block/Square (52), International Money Express (56), UnionPay (49), JCB (39).

Moving up but not exiting: Visa (now 52, was 43).

Net direction: Stable. The Q1 framework's most-cited paradox — Visa, UnionPay, and JCB as open but unresolved networks — remains intact. Visa's +9 drift is the only meaningful movement within the archetype.

Closed or Sovereign Holders (Blocked posture, ECC = 0)

Held position: Mastercard, Global Payments, Worldline, Toast, Coinbase.

Net direction: Stable. None of the Q1 Blocked members re-entered AI legibility in Q2. This is different from the Media Q2 reading (where Al Jazeera re-entered, +66), the Finance Q2 reading (where Marsh & McLennan re-entered, +65), and the eCommerce Q2 reading (where eBay re-entered, +60). Payments Closed Holders appear to be more durably committed to their Blocked positions than the equivalent archetypes in other sectors.

The strategic interpretation: payments Blocked positions are more often regulatory or competitive infrastructure decisions (Mastercard's network monetization, Coinbase's regulatory posture) rather than experimental or reversible choices. The framework should note this difference when interpreting cross-sector Blocked archetype dynamics.

Index

Strategic Implications

Q1 Payments framed documentation culture as the predictive variable for AI legibility — the structural finding that distinguished payments from media, finance, and other verticals. Q2 sharpens that framing in four ways.

Authority Compounder status is operationally fragile. Ramp's -62 ECC collapse from Authority Compounder to Open but Unresolved demonstrates that the structural infrastructure supporting High capability ratings can be erased within a single quarter. Documentation discipline produces AI legibility; disruption to that discipline (site restructuring, schema migration, content revision, brand repositioning) can remove it just as quickly. For the 16 firms remaining in the Authority Compounder archetype, this is a warning: the archetype is not a destination, it is a state that requires continuous maintenance.

The network paradox is partially closing — but slowly. Visa's +9 drift suggests the largest payments network in the world is beginning to address its Q1 AI-legibility gap. Mastercard's flat reading at 0 suggests the gap between the two duopoly partners is widening for the first time in their competitive history. If Visa continues its trajectory in Q3 and reaches ECC 60+ by Q4, AI-mediated payments recommendation queries will increasingly favor Visa over Mastercard for explanation, comparison, and citation. This is the first measurable structural divergence between the two networks in the Q1/Q2 datasets, and it is moving in only one direction.

The cross-border money-movement segment is structurally advantaged. dLocal, Green Dot, Flywire, and the broader money-movement cohort (Wise, Remitly, Payoneer, Western Union) continue to outperform the network and processor segments. The Q1 framework attributed this to regulatory documentation requirements and developer-first API culture. Q2 reinforces the pattern. For payments executives, the strategic implication is clear: if the firm operates in cross-border or alternative payments, the AI-legibility tailwind is real. If the firm operates in network or processor infrastructure, the tailwind is much weaker and requires deliberate investment to capture.

The crypto AI-legibility advantage requires re-examination. Circle's -10 drop and Fireblocks' -6 drift introduce a question the Q1 framework did not need to ask: is the crypto sector's exceptional Q1 AI-legibility a durable structural advantage, or a transient state tied to a specific regulatory moment? The Q1 thesis was that stablecoin regulatory clarity requirements produce AI-legibility as a byproduct. If Q3 shows continued negative drift in Circle and Fireblocks, the regulatory-clarity-as-AI-legibility thesis will need partial revision. If Q3 shows recovery, the Q2 drift was tactical.

The strategic question for payments executives is no longer whether documentation culture matters — Q2 confirms it does. The question is whether the firm's documentation discipline is structurally durable enough to survive normal operational changes (site updates, rebrands, platform migrations) without losing the AI-legibility it has built. Ramp just provided the negative example. The other Authority Compounders should treat that as a planning data point.

Full Report

Payments' AI thesis was the sharpest of the Q1 baseline reports: documentation culture predicts AI legibility better than market dominance. Q2 leaves the central thesis intact while introducing one major exception and one quiet structural shift.

The Ramp collapse is the largest negative ECC move in any Q2 reading. Ramp moved from Open/High/80 to Open/Low/18 — a -62 ECC drop with capability falling two tiers from High to Low. The Q1 framework named Ramp as one of seven developer-first private fintechs (Stripe, Checkout.com, Fireblocks, Rapyd, Plaid, Brex, Ramp) that anchored the documentation-culture thesis. The other six held position or drifted modestly. Ramp's collapse is therefore an isolated structural event within a group that otherwise demonstrated the Q1 thesis was holding.

The strategic implication matters more than the numerical drop. The Q1 framework treated Authority Compounder status as the natural product of sustained documentation discipline. Ramp's Q2 reading demonstrates that this status is operationally fragile: a major site restructuring, schema migration, brand repositioning, or content revision can erase the structural infrastructure that produced the original High capability rating. For the other 16 Authority Compounders in the dataset, this is a planning data point. Documentation discipline produces AI legibility, but the link between the two is more fragile than the Q1 framework suggested.

Three possible explanations for the Ramp drop exist, and the Q3 reading will distinguish among them. If Ramp recovers to ECC 60+ in Q3, the Q2 reading captured a discrete transition event. If Ramp stays at ECC 18, the Q2 reading captured a structural decision. If Ramp returns to the 80s, Q1 was the anomaly. None of these outcomes individually resolves the broader question about Authority Compounder durability — but the trajectory will indicate how concerned the framework should be about similar future events.

The Visa +9 drift is the quietest structurally important move in any Q2 reading. Visa moved from ECC 43 to ECC 52, no posture change, no capability change. In isolation, the move is unremarkable. In context, it is the first measurable evidence that the network paradox the Q1 framework identified is beginning to close.

Visa is the largest payments network in the world by transaction volume. The Q1 framework recorded its ECC at 43 — Low capability, Open but Unresolved archetype — and used that score as the marquee example of how operational dominance does not translate into AI-layer authority. Q2's +9 drift indicates that Visa is doing documentation work that simply was not happening in Q1. The magnitude is small. The trajectory is the data point.

Mastercard's contrast is sharp. Visa moved +9. Mastercard held at 0. Two networks that have historically operated as a duopoly with rough strategic parity now show measurable divergence in their AI-legibility trajectories. If Visa continues at this pace in Q3 and Q4, the AI-mediated payments recommendation landscape will increasingly favor Visa for explanation, comparison, and citation. Mastercard's structural disadvantage will compound as Visa's structural advantage accumulates.

The Q3 question for Mastercard is whether the Q1 strategic decision to maintain Blocked posture remains optimal given the Q2 evidence that Visa is moving in the opposite direction. If Mastercard holds Blocked through Q3 and Q4, the duopoly will have measurably broken in AI-mediated discovery — a meaningful first in financial infrastructure competitive history.

The dLocal and Green Dot promotions confirm the money-movement thesis. dLocal moved from Open/Medium/67 to Open/High/90 (+23). Green Dot moved from Open/Medium/69 to Open/High/86 (+17). Both companies now sit in the Authority Compounder archetype. The Q1 framework's segment analysis showed Money Movement as the highest-ECC payments segment (average ECC 74.4, 57% High Capability) — Q2 reinforces this finding decisively.

dLocal specifically deserves direct attention. Now at ECC 90, dLocal is the second-highest-scored entity in the Q2 Payments dataset behind only Fireblocks (85, drifted down from 91). dLocal's focus on emerging-market cross-border payments means a Latin American specialist has now reached top-tier Authority Compounder status — the first such entity to do so in any Q2 ECC reading. The geographic distribution of Authority Compounder status is broadening, and dLocal is the cleanest example.

Green Dot's +17 gain is more domestic in character but structurally similar. The firm operates in alternative banking and money-movement services for unbanked and underbanked US consumers — a category that the Q1 framework treated as a Commodity Retail Pipe equivalent in eCommerce but that the Payments framework correctly placed in Money Movement. Green Dot's Q2 promotion to Authority Compounder validates the Q1 segment assignment.

The crypto Authority Compounders drifted negatively, raising a Q3 question. Circle moved from Open/High/83 to Open/Medium/73 (-10, capability dropped from High to Medium). Fireblocks moved from Open/High/91 to Open/High/85 (-6, capability held). The Q1 framework identified crypto infrastructure as showing "extreme divergence" — Coinbase blocked while Circle and Fireblocks were among the clearest entities in the dataset. The Q1 explanation was that regulatory-clarity requirements for stablecoins produce AI-legibility as a byproduct.

Q2 introduces a question the Q1 framework did not need to address: is the crypto AI-legibility advantage durable, or is it tied to a specific regulatory moment that may be passing? Circle's High → Medium capability drop is the more important signal of the two. Fireblocks' -6 ECC at constant High capability suggests smaller adjustments. Circle's larger move suggests structural changes.

If Q3 shows continued negative drift, the Q1 thesis on crypto-as-AI-legibility-leader will require partial revision. If Q3 shows recovery, the Q2 drift was tactical and the Q1 thesis remains intact.

The Nuvei posture change introduces a fifth posture-experimentation example with a structural difference. Nuvei moved from Defensive/Medium/64 to Open/Medium/73 — a +9 ECC gain with posture moving from Defensive to Open. This is the fifth cross-sector example of posture experimentation (after American Express, Nu Holdings, Publicis Sapient, and Burlington Stores). But Nuvei's case is structurally different from the previous four: the posture change accompanied a measurable ECC gain.

This may indicate two distinct types of posture experimentation:

- Experimental — posture changes at constant ECC and capability (the four previous examples), where the institution is testing whether the access posture itself affects downstream outcomes without committing to underlying structural changes.

- Structural — posture changes with accompanying ECC and capability gains (Nuvei), where the institution made a deliberate decision to open more deeply and invested in the documentation infrastructure to make that opening productive.

If more firms make Nuvei-style structural posture changes in Q3, the framework will need to formally distinguish between these two patterns. The strategic implications are different: experimental posture changes are reversible and tactical; structural posture changes are commitments to a new AI-legibility position.

The American Express case extends the conglomerate disaggregation pattern. American Express appears in this Payments dataset and the Finance dataset with different Q1 starting postures and different Q2 trajectories. In Payments, AmEx held at Open/Medium/68 across both quarters. In Finance, AmEx moved from Defensive to Open at the same ECC 68 — a posture experimentation move identified in the Finance Q2 report.

This is the second documented case of a parent entity appearing in two ECC reports with divergent operational trajectories. Marsh McLennan was the first (Q2 Finance vs. Q2 Consulting). The pattern now has cross-sector evidence: large multi-line financial services firms make different AI strategy decisions for different surfaces of their business. The framework should consider whether Q3 reporting needs to formally track corporate vs. operational AI postures separately when material divergence is observable.

Six questions will frame the Q3 reading on Payments:

- Does Ramp recover, hold at 18, or normalize at a middle level? The answer determines whether Authority Compounder status is durable or fragile.

- Does Visa continue its +9 trajectory? Continued positive movement would indicate the network paradox is closing structurally rather than tactically.

- Does Mastercard remain at 0 while Visa moves, or does Mastercard finally respond? The duopoly divergence is the most important strategic question in payments infrastructure.

- Do Circle and Fireblocks recover, or does the crypto AI-legibility thesis require revision?

- Does dLocal hold ECC 90, or does it normalize down? If it holds, the geographic broadening of Authority Compounder status is durable.

- Do additional firms make Nuvei-style structural posture changes (Defensive → Open with ECC gain)? Or does the posture-experimentation pattern remain primarily tactical?

The Q1 Payments thesis is largely intact. Documentation culture predicts AI legibility better than market dominance. Money-movement firms outperform networks. Crypto infrastructure has been exceptionally legible. Networks remain invisible or unresolved. What Q2 adds is the operational fragility of Authority Compounder status (Ramp), the beginning of the network paradox closure (Visa), and the structural rather than experimental form of posture change (Nuvei). The framework's core insight stands. Its operational nuances now have more texture.