Entity Clarity Report — Professional Services & Consulting in the AI Era: Q2 2026 Update

Summary

The Q1 Consulting thesis — that firms selling execution are being repriced while firms retaining judgment show durable authority — is now empirically observable. In Q2, four firms gained High capability through deliberate investment (BCG, Roland Berger, Capgemini, Slalom). Two firms that historically sold execution retreated into Blocked posture (TCS, Willis Towers Watson). The bifurcation the Q1 report predicted is happening on schedule, and it is happening along exactly the judgment-versus-execution line the framework identified.

Methodology

No changes to the ECC framework were made for Q2.

Posture definitions, capability tiers, and the three weighted ECC components — Entity Comprehension & Trust, Structural Data Fidelity, and Page-Level Hygiene — remain as published in the Q1 report.

One methodology note relevant to Q2 Consulting movement: a Blocked posture produces an ECC of 0 by definition, not by measurement. When a firm prevents AI systems from crawling its surfaces, the framework has nothing to score. Several of the largest Q2 negative moves in Consulting are Blocked transitions — these reflect strategic choices, not capability collapses. The strategic question the framework is designed to surface is whether the Blocking decision reflects offensive IP protection (the Bloomberg/People pattern) or defensive retreat from AI substitution (a new pattern visible in this dataset).

Quarterly cadence continues. The Q3 update will publish following Q3 2026 close.

See details on the 13-signal framework

Findings

Five findings emerge from the Q2 Consulting reading.

1. The judgment cluster is compounding faster than predicted

The Q1 framework identified firms retaining judgment as the durable winners in AI-mediated consulting markets. Q2 provides concrete evidence: four firms moved up a full capability tier in one quarter, and three of them (BCG, Roland Berger, Capgemini) reached or approached the top of the entire Consulting dataset.

Capgemini's move to ECC 97 is the most striking. It is now the highest-scoring institution in any of the Q2 ECC readings — higher than Citigroup's Q1 Finance peak (88), higher than Sky News's Q1 Media peak (86), tied with KLA's Tech 100 score (92). For a firm in IT/Management Consulting — historically positioned closer to execution than to judgment — to reach the top of the dataset suggests a deliberate strategic reframe.

BCG's move from Medium to High capability is structurally significant. The Q1 framework placed BCG in the strategy consulting tier alongside Bain and L.E.K., but with lower ECC and lower capability. Q2 closes that gap. BCG, Bain, and L.E.K. now sit within ECC 81-83 with High capability — a coherent peer group of strategy firms positioned as judgment institutions.

Roland Berger's +20 ECC gain to 89 is the largest pure ECC move in the Consulting Q2 dataset and one of the largest in any Q2 reading. Combined with its move from Medium to High capability, this signals deliberate restructuring of its AI-legibility infrastructure — likely a response to losing ground to McKinsey and BCG in AI-mediated brand searches.

The Q3 question for this cluster: do BCG, Roland Berger, Capgemini, and Slalom hold their new capability tiers, or do they require continuous investment to maintain them? The Q1 Tech reading (Applied Materials exit) demonstrated that high ECC is not durable by default. Whether judgment-tier capability behaves the same way will be visible in Q3.

2. The TCS retreat is a new strategic pattern

Tata Consultancy Services moved from Defensive/Medium/68 to Blocked/Low/0 in one quarter. This is the largest negative move in the Q2 Consulting dataset and one of the largest cross-sector reversals.

The strategic interpretation is different from any previous Q2 Blocked migration. TCS is not Bloomberg (premium financial IP). TCS is not People (flagship media asset). TCS is not Sky News (Sovereign withdrawal). TCS is an IT services firm whose business model historically depended on selling execution at scale — exactly the function the Q1 framework predicted would be repriced by AI.

The TCS Blocked decision is most likely a defensive retreat: if AI systems can summarize, contextualize, and increasingly replicate IT services interpretation, allowing those systems to crawl and learn from TCS's surfaces accelerates the firm's own commoditization. Blocking AI does not solve the substitution problem, but it slows the rate at which AI systems can describe TCS's competitors as superior alternatives.

This is the first cross-sector Q2 example of Blocking used as defensive retreat from substitution risk, distinct from offensive IP protection. The pattern is worth naming: Substitution-Defensive Blocking. Watch for similar moves in Q3 from other execution-dependent firms — IT outsourcing, back-office services, certain BPO categories.

3. The Willis Towers Watson reversal challenges the insurance-broker framing

Willis Towers Watson moved from Open/High/80 to Blocked/Low/0 — a -80 ECC drop, the largest in the Q2 Consulting reading.

The move is strategically harder to read than TCS. WTW is an insurance broker and risk advisory firm — closer to the advisory-adjacent category that the Q2 Finance reading identified as poorly suited for Blocked posture (where Marsh & McLennan re-entered AI legibility from Blocked, +65). WTW is moving in the opposite direction from its closest peer.

Three interpretations are possible:

One: WTW is making a different strategic bet than Marsh — perhaps protecting proprietary risk modeling and actuarial frameworks that the firm believes have direct licensing value.

Two: WTW is making a defensive retreat similar to TCS — treating insurance brokerage execution as substitutable and trying to slow the rate of AI-enabled competitive substitution.

Three: WTW is making a strategic error that the Q3 reading will eventually reveal.

The framework cannot distinguish among these from a single quarterly reading. What is clear is that Marsh & McLennan and WTW — two large insurance brokerage firms with overlapping business models — chose opposite postures within the same quarter. This is the cleanest test the Q1 framework has yet faced: if WTW gains relative AI authority in Q3 by being Blocked, the Alpha Fortress logic applies to advisory-adjacent firms. If Marsh gains relative AI authority by being Open, the substitution-defensive logic applies. One of these firms will be empirically wrong by Q4.

4. Marsh McLennan demonstrates the conglomerate-disaggregation pattern

Marsh McLennan appears in both the Finance and Consulting datasets — in Finance as the parent insurance brokerage entity, in Consulting as the firm's advisory operations (which include Mercer, Oliver Wyman, and Guy Carpenter). The Q1 baseline scored these separately, and the Q2 reading shows them moving differently.

In the Finance dataset, Marsh & McLennan moved from Blocked/Low/0 to Open/Medium/65 (+65). In the Consulting dataset, Marsh McLennan moved from Open/Low/56 to Open/Medium/65 (+9). The same conglomerate produced different ECC trajectories in different functional domains.

This is structurally important for the framework. The Q1 reports assumed institutions could be evaluated as single entities. Q2 demonstrates that large conglomerates have multiple AI-legibility profiles depending on which functional operation is being measured. Marsh McLennan's parent-entity AI surfaces (corporate communications, investor relations, integrated risk) made a different strategic choice than its advisory operations' AI surfaces (Mercer thought leadership, Oliver Wyman insights, Guy Carpenter analysis).

The Q3 question: does the disaggregation persist or converge? If conglomerates increasingly align their AI strategy across functional units, the framework's per-entity measurement remains accurate. If conglomerates continue to make different choices across functional units, the framework may need to formally distinguish between corporate AI postures and operational AI postures.

5. The Big Four split: KPMG drift signals possible category shift

KPMG Advisory moved from Open/Medium/74 to Open/Medium/67 — a -7 ECC drift within the same posture and capability tier. This is small in isolation but meaningful in context: KPMG was the only Big Four advisory entity to move negatively in Q2. PwC Advisory remained at 0 (Blocked). EY-Parthenon held at ECC 81 (Open/High). Deloitte Consulting held at ECC 68 (Defensive/Medium). Strategy& (PwC) held at 0 (Blocked).

The Big Four advisory market has historically operated as a peer set with rough strategic parity. Q2's drift suggests that parity is dissolving. EY-Parthenon's High capability now positions it ahead of its Big Four peers as the strategic-tier consulting brand. Deloitte's Defensive posture suggests controlled exposure rather than judgment leadership. PwC and Strategy& continue to use Blocking as the primary strategy. KPMG's drift suggests the firm has not yet chosen — and indecision is now visible as ECC loss.

If KPMG continues to drift in Q3, the Big Four advisory market may functionally split into three groups: judgment leaders (EY-Parthenon), controlled-exposure stewards (Deloitte), and IP-protective blockers (PwC, Strategy&). KPMG would face a strategic choice about which of these three positions to occupy.

Landscape

The Q1 Consulting report opened with a thesis that is now being tested in real time: consulting firms historically monetized three things — interpretation, execution, and permission — and AI now performs the first two at near-zero marginal cost. The Q1 framework predicted that firms selling execution would be repriced and firms retaining judgment would show durable authority.

Q2 confirms both predictions earlier than expected.

Judgment is compounding. Four firms gained a full capability tier in one quarter. BCG moved from Medium to High capability (ECC 65 → 82, +17). Roland Berger moved from Medium to High (ECC 69 → 89, +20). Capgemini gained ECC 14 points to 97, the highest score in the Consulting dataset. Slalom moved from Medium to High capability (ECC 67 → 81, +14). These are not drift movements — they are deliberate investments in the structural infrastructure that signals interpretive authority to AI systems.

Execution is retreating. Two firms that historically sold execution moved into Blocked posture. TCS (Tata Consultancy Services) moved from Defensive/Medium/68 to Blocked/Low/0 — a -68 ECC drop. Willis Towers Watson moved from Open/High/80 to Blocked/Low/0 — a -80 ECC drop, the second-largest single-quarter ECC reversal in any Q2 ECC reading (behind only Sky News in Media).

The Q1 framework treated Blocking as a single strategic posture. Q2 Consulting demonstrates that Blocking now means two different things depending on the firm's underlying business model. McKinsey and Strategy& block AI because their core product is proprietary judgment delivered to paying clients — their Blocked posture is offensive IP protection. TCS and WTW block AI because their core product is increasingly substitutable by AI — their Blocked posture is defensive retreat from substitution risk.

This distinction matters. The defensive-retreat pattern is new to the Q2 dataset across all sectors, and Consulting is where it is most clearly visible.

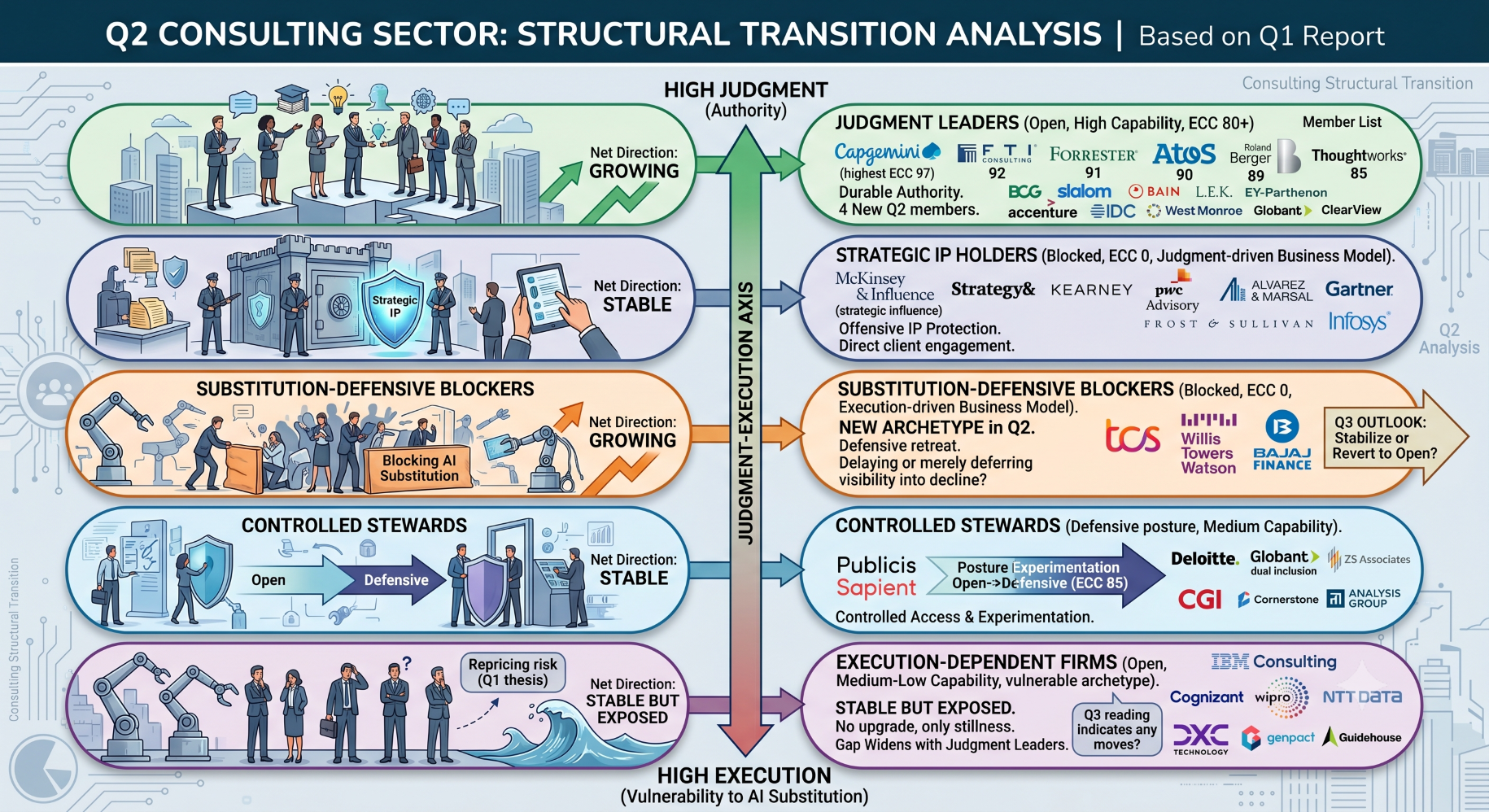

Archetypes

The Q1 Consulting report identified the sector as being in structural transition along the judgment-execution axis. Q2 sharpens the archetype categories that organize that transition.

Judgment Leaders (Open, High capability, ECC 80+)

Joined in Q2: BCG (Defensive/High/82), Roland Berger (Open/High/89), Capgemini (Open/High/97), Slalom (Defensive/High/81).

Held position: Bain (81), L.E.K. (83), EY-Parthenon (81), Accenture (81), Atos (90), Forrester (91), IDC (80), West Monroe (80), Thoughtworks (85), Globant (83), ClearView Healthcare Partners (82), FTI Consulting (92).

Net direction: Growing. The Judgment Leader archetype gained four members in one quarter, including Capgemini at the highest ECC in the dataset. This is the archetype the Q1 framework predicted would show durable authority. Q2 confirms.

Strategic IP Holders (Blocked, ECC 0, judgment-driven business model)

Held position: McKinsey, Strategy&, Kearney, PwC Advisory, Alvarez & Marsal, Gartner, Frost & Sullivan, Infosys.

Net direction: Stable. These are firms whose judgment is the product and whose blocking is offensive IP protection. The Q1 archetype description remains accurate. McKinsey in particular continues to demonstrate that Blocked posture is compatible with maximum strategic influence when the firm's primary product is delivered through direct client engagement rather than AI-mediated discovery.

Substitution-Defensive Blockers (Blocked, ECC 0, execution-driven business model)

New archetype in Q2. Members: TCS (newly Blocked), Willis Towers Watson (newly Blocked), EPAM Systems (held Blocked), Bajaj Finance (in Finance dataset).

Net direction: Growing. This is the new archetype the Q1 framework did not articulate. These are firms whose Blocking posture appears to be defensive retreat from AI substitution rather than offensive IP protection. The strategic question for this group is whether Blocking actually slows substitution or merely defers visibility into the substitution that is already happening.

Q3 will indicate whether this archetype stabilizes or whether members revert to Open postures once the futility of substitution-defensive blocking becomes apparent.

Controlled Stewards (Defensive posture, Medium capability)

Held position: Deloitte Consulting (68), Globant (83), CGI Group (66), Cornerstone Research (61), Analysis Group (78), ZS Associates (57), Publicis Sapient (newly Defensive at 85).

Notable move: Publicis Sapient shifted from Open/High/86 to Defensive/High/85. Same capability, same approximate ECC, different posture. This is the Consulting-sector example of the posture-experimentation pattern visible in the Q2 Finance reading (American Express, Nu Holdings).

Net direction: Stable, with one new entrant experimenting at the margin.

Execution-Dependent Firms (Open, Medium-Low capability, vulnerable archetype)

Held position: IBM Consulting (61), Cognizant (53), Wipro (73), DXC Technology (68), NTT Data (65), Genpact (63), Guidehouse (61).

Net direction: Stable but exposed. These are the firms most directly in the path of the Q1 thesis. None upgraded to High capability in Q2. None retreated to Blocked. The Q1 framework predicted this group would be "repriced" — Q2 shows no evidence of upgrade or retreat, only stillness.

The strategic question: at what point does stillness in this archetype become measurable as relative decline? Each quarter that the Judgment Leaders compound and these firms hold position, the gap widens. The Q3 reading will indicate whether any firms in this archetype move in either direction.

Index

Strategic Implications

Q1 Consulting framed the sector as being decomposed function by function. Q2 sharpens that framing in four ways.

Judgment is investable, not assumed. Four firms gained a full capability tier in one quarter through deliberate structural investment. This was not drift. Capgemini's move to ECC 97 required schema work, content restructuring, entity disambiguation, and aggressive lattice-building. The framework now treats Judgment Leader status as the product of measurable investment decisions rather than inherited brand equity. Firms that want to compete in this archetype must invest in the underlying infrastructure; reputation alone is insufficient.

Blocking is now operationally bifurcated. McKinsey blocks AI to protect proprietary judgment delivered to paying clients. TCS blocks AI to slow substitution risk. Both produce an ECC of 0 in the framework, but the strategic underlying positions are opposite. The Q3 framework will likely need to formally distinguish between Strategic IP Holders and Substitution-Defensive Blockers. The two groups are not interchangeable for analytical purposes, and the long-term outcomes for each are likely to diverge significantly.

The conglomerate disaggregation matters for the framework. Marsh McLennan demonstrates that a single corporate entity can produce different AI-legibility profiles across functional operations. This was not visible in Q1 because the framework treated each entity as a single unit. Q2 indicates that for large conglomerates, AI strategy may now be set at the operating-unit level rather than the corporate level. The framework should consider whether Q3 reporting needs to track conglomerate operations separately when material divergence is observable.

The Willis Towers Watson and Marsh McLennan divergence is the cleanest natural experiment in the Q2 dataset. Two insurance brokerage firms with overlapping business models chose opposite AI postures within the same quarter. The Q3 and Q4 readings will provide near-controlled experimental data on which posture produces better AI-mediated outcomes for advisory-adjacent insurance firms. This is the kind of natural experiment that retroactively validates or refutes framework predictions, and it is worth tracking explicitly across the next two quarterly readings.

The strategic question for consulting executives is no longer whether AI affects their business model — Q2 confirms it already has. The question is whether the firm's AI posture matches the firm's actual product. Firms selling judgment should be optimizing for legibility. Firms selling execution face a choice: invest in judgment infrastructure to migrate up the archetype ladder, or accept the substitution risk that Blocking only partially defers. The middle position — open but unreadable, open but uninvested — is no longer viable.

Full Report

Consulting's AI thesis was the sharpest of the Q1 baseline reports: firms selling execution are being repriced, firms retaining judgment show durable authority, the industry is being decomposed function by function. Q2 makes that thesis empirically observable.

The judgment cluster compounded. Four firms gained a full capability tier in one quarter. BCG (Defensive/High/82, +17 ECC). Roland Berger (Open/High/89, +20 ECC). Capgemini (Open/High/97, +14 ECC). Slalom (Defensive/High/81, +14 ECC). Capgemini's move to ECC 97 is the highest score in any Q2 ECC reading across Tech, Media, Finance, and Consulting. For an IT/Management Consulting firm historically positioned closer to execution than to judgment, that score signals a deliberate strategic reframe. BCG's move closes the capability gap with Bain and L.E.K., creating a coherent strategy-tier peer set at ECC 81-83. Roland Berger's +20 is the largest pure ECC gain in the Consulting Q2 dataset and one of the largest in any Q2 reading.

These moves are not drift. They are investment outcomes. Each of the four firms made measurable structural changes to its AI-legibility infrastructure within the quarter — schema work, entity disambiguation, lattice-building, content restructuring. The framework records the result, but the strategic decision sits upstream: these firms decided that being read as judgment institutions was worth the operational cost of being read clearly.

The execution cluster retreated. Two firms whose business models depended on selling execution at scale moved into Blocked posture. TCS (Tata Consultancy Services) moved from Defensive/Medium/68 to Blocked/Low/0 — a -68 ECC drop. Willis Towers Watson moved from Open/High/80 to Blocked/Low/0 — a -80 ECC drop, the second-largest single-quarter ECC reversal in any Q2 ECC reading.

These moves require a new analytical category. McKinsey's Blocked posture (ECC 0 since Q1) is offensive: it protects the firm's proprietary judgment from being summarized and given away. The Q1 framework treated all Blocked postures this way. TCS and Willis Towers Watson are doing something different. Both firms operate in markets where AI is becoming a direct substitute for the firm's primary product — IT services execution and insurance brokerage advisory, respectively. Their Blocked moves do not protect proprietary judgment; they slow the rate at which AI systems can describe their services as substitutable.

This is Substitution-Defensive Blocking — a new archetype not articulated in the Q1 framework. The strategic logic is different from the Q1 Alpha Fortress logic, and the long-term outcome is likely different. Alpha Fortresses (S&P Global, CME Group, Mastercard) sell verified scarcity through controlled access. Substitution-Defensive Blockers sell execution that AI can increasingly replicate. The first group's Blocked posture compounds value. The second group's Blocked posture defers visibility into a substitution problem that does not actually go away. Q3 will indicate which firms in this category continue down the Blocked path and which reverse course.

The Marsh McLennan disaggregation is the framework's first clear signal that conglomerates now require multi-entity treatment. Marsh McLennan appears in the Q2 Finance dataset moving from Blocked/Low/0 to Open/Medium/65 (+65). It also appears in the Q2 Consulting dataset moving from Open/Low/56 to Open/Medium/65 (+9). The same parent entity produced opposite Q1 starting postures and different Q2 trajectories depending on whether the framework measured corporate-entity AI surfaces or advisory-operation AI surfaces. The advisory side (Mercer, Oliver Wyman, Guy Carpenter) made a smaller, steadier upward move. The parent-entity side made a larger reversal move.

The Q1 reports implicitly assumed each entity could be evaluated as a single unit. Q2 demonstrates this assumption breaks for large conglomerates. The strategic implication is that AI strategy in multi-line firms may now be set at the operating-unit level rather than the corporate level — and that the framework needs to track these separately when material divergence is observable. The Q3 update may need a methodology revision to formalize conglomerate disaggregation.

The Willis Towers Watson and Marsh McLennan divergence is the cleanest natural experiment in the Q2 dataset across any sector. Two large insurance brokerage firms with substantially overlapping business models, advisory products, client bases, and competitive positioning chose opposite AI postures within the same quarter. WTW went from Open/High to Blocked. Marsh McLennan moved from Blocked toward Open. One of these decisions will be empirically validated by Q3 and Q4 outcomes; the other will be empirically refuted. There are very few moments in strategic frameworks where competing hypotheses can be tested this directly. The exmxc.ai framework should track this divergence as a defined experiment with explicit Q3 and Q4 evaluation criteria.

The KPMG drift is a quieter signal of category dissolution. KPMG Advisory moved from Open/Medium/74 to Open/Medium/67 — a -7 ECC drift, no posture change, no capability change. In isolation, this is unremarkable. In context, it is the only Big Four advisory entity to lose ground in Q2. EY-Parthenon held at 81. Deloitte Consulting held at 68. PwC Advisory and Strategy& held at 0. The Big Four advisory market historically operated as a peer set with rough strategic parity; Q2's drift suggests that parity is dissolving into three distinct positions: judgment leadership (EY-Parthenon), controlled exposure (Deloitte), IP-protective blocking (PwC, Strategy&). KPMG has not yet chosen, and indecision is now visible as measurable ECC loss.

The Publicis Sapient posture shift confirms the Q2 Finance pattern. Publicis Sapient moved from Open/High/86 to Defensive/High/85 — same capability, near-identical ECC, different posture. This is the Consulting-sector example of the posture experimentation pattern that American Express and Nu Holdings demonstrated in the Q2 Finance reading. Firms are testing whether posture changes at constant capability produce different downstream outcomes (citation patterns, partner inquiry volume, competitive substitution rates). If this pattern continues into Q3 across multiple sectors, the framework will need to distinguish experimental posture changes from structural commitments.

Six questions will frame the Q3 reading on Consulting:

- Do the four new Judgment Leaders (BCG, Roland Berger, Capgemini, Slalom) hold their capability gains, or does Judgment Leader status require continuous investment to maintain?

- Does Substitution-Defensive Blocking spread to other execution-dependent firms — additional IT services, BPO categories, insurance advisory, certain accounting functions?

- Does WTW gain relative authority by being Blocked, or does Marsh McLennan gain relative authority by being Open? The Q3/Q4 readings on these two firms will validate or refute the Substitution-Defensive Blocking thesis.

- Does the Marsh McLennan conglomerate disaggregation pattern appear in other large multi-line firms — Accenture, Deloitte, IBM, Capgemini — when measured at operating-unit level?

- Does KPMG choose a category in Q3, or continue drifting? Continued drift signals strategic indecision that the framework can now measure.

- Do the Execution-Dependent Firms (Cognizant, IBM Consulting, DXC, NTT Data, Genpact) show any movement, or does their Q2 stillness persist? Stillness in this archetype is itself becoming measurable as relative decline.

The Q1 Consulting thesis is no longer a hypothesis. It is an observation. Firms selling judgment are compounding. Firms selling execution are either upgrading judgment infrastructure to escape the substitution path or retreating into Blocked posture to defer visibility into substitution. The middle position — open, mid-capability, uninvested — has been depopulated of upward-moving members in Q2. The next two quarters will indicate whether the bifurcation completes or stalls.