Entity Clarity Report — Technology in the AI Era: Q2 2026 Update

Summary

One quarter after the Q1 baseline, 17 of the Tech 100 moved. Most shifts are recalibrations within the same archetype. A handful are structural — including one company's deliberate exit from the AI judgment layer. This update records the first quarterly reading against the Q1 baseline and identifies where the AI-mediated authority layer is moving fastest.

Methodology

No changes to the ECC framework were made for Q2.

Posture definitions, capability tiers, and the three weighted ECC components — Entity Comprehension & Trust, Structural Data Fidelity, and Page-Level Hygiene — remain as published in the Q1 report.

One methodology note worth restating: a Blocked posture produces an ECC of 0 by definition, not by measurement. When a company prevents AI systems from crawling its surfaces, the framework has nothing to score. This is recorded as a strategic choice, not a capability failure.

Quarterly cadence will continue. The Q3 update will publish following Q3 2026 close.

See Entity Clarity Framework for Rubric

Findings

Three findings emerge from the first quarterly reading.

1. The Applied Materials decision is the largest single signal of Q2

Applied Materials moved from ECC 91 — the second-highest score in the entire Q1 index — to ECC 0 in a single quarter. The company shifted posture from Defensive to Blocked.

This is not a capability collapse. Applied Materials chose to stop allowing AI systems to crawl its surfaces. Under the ECC framework, a Blocked posture produces a score of 0 by definition: when a company opts out of being read, there is nothing for the methodology to score.

The decision is the data. A company that ranked among the top three Authority Compounders in Q1 has now joined the Closed or Sovereign Holders. This is the first quarter-over-quarter exit from the Authority Compounder tier in any ECC report.

The implication is not about Applied Materials' AI capability — it is about its judgment regarding the cost of being interpreted. In Q1, the company was willing to be read. In Q2, it was not. The Q3 reading will indicate whether this is durable or reversible.

2. Megacap drift is consistently negative; mid-cap drift is consistently positive

Alphabet, Amazon, and Intel — three of the largest non-Apple, non-NVIDIA Open-posture US entities — all lost ECC ground in Q2. None catastrophically. All in the same direction.

Meanwhile, Adobe (+14), Advantest (+14), Constellation Software (+17), Robinhood (+8), Schneider Electric (+8), Keyence (+6), and Datadog (+6) all gained. The infrastructure and software middle of the index is doing the documentation and entity work that megacaps are not.

If this pattern persists in Q3, the assumption that scale protects authority will need to be formally retired.

3. Asian mid-caps are the most mobile cohort

Three of the most significant positive moves in Q2 came from Asian companies: SK Hynix unblocked from 0 to 48, Trip.com gained capability (+24), and Advantest gained capability (+14).

This is a small sample, but it points at a possible geographic re-weighting of ECC over the coming quarters. The Q3 reading will indicate whether this cluster keeps moving.

Landscape

Movement in Q2 clusters into three categories: structural shifts, drift, and consolidation.

Structural shifts are full archetype reclassifications — posture and capability both moved, or a company crossed the Authority Compounder threshold. Four companies moved structurally in Q2.

Drift describes smaller ECC moves within the same posture and archetype. These are the slow stories — the ones that compound or reverse over multiple quarters. Fourteen companies drifted in Q2.

Consolidation describes companies that held position. Eighty-three entries did not move. This is signal, not noise. The framework measures posture and capability, both of which are slow-moving by design. A high churn rate would suggest the methodology was capturing noise rather than position.

The stability of the Closed and Sovereign tier — every Q1 Blocked company except SK Hynix remained Blocked — confirms the framework is detecting strategic positioning rather than tactical adjustment.

Archetypes

The five archetypes from Q1 remain unchanged. What changed in Q2 is which companies sit inside them.

Authority Compounders (ECC ≥ 80)

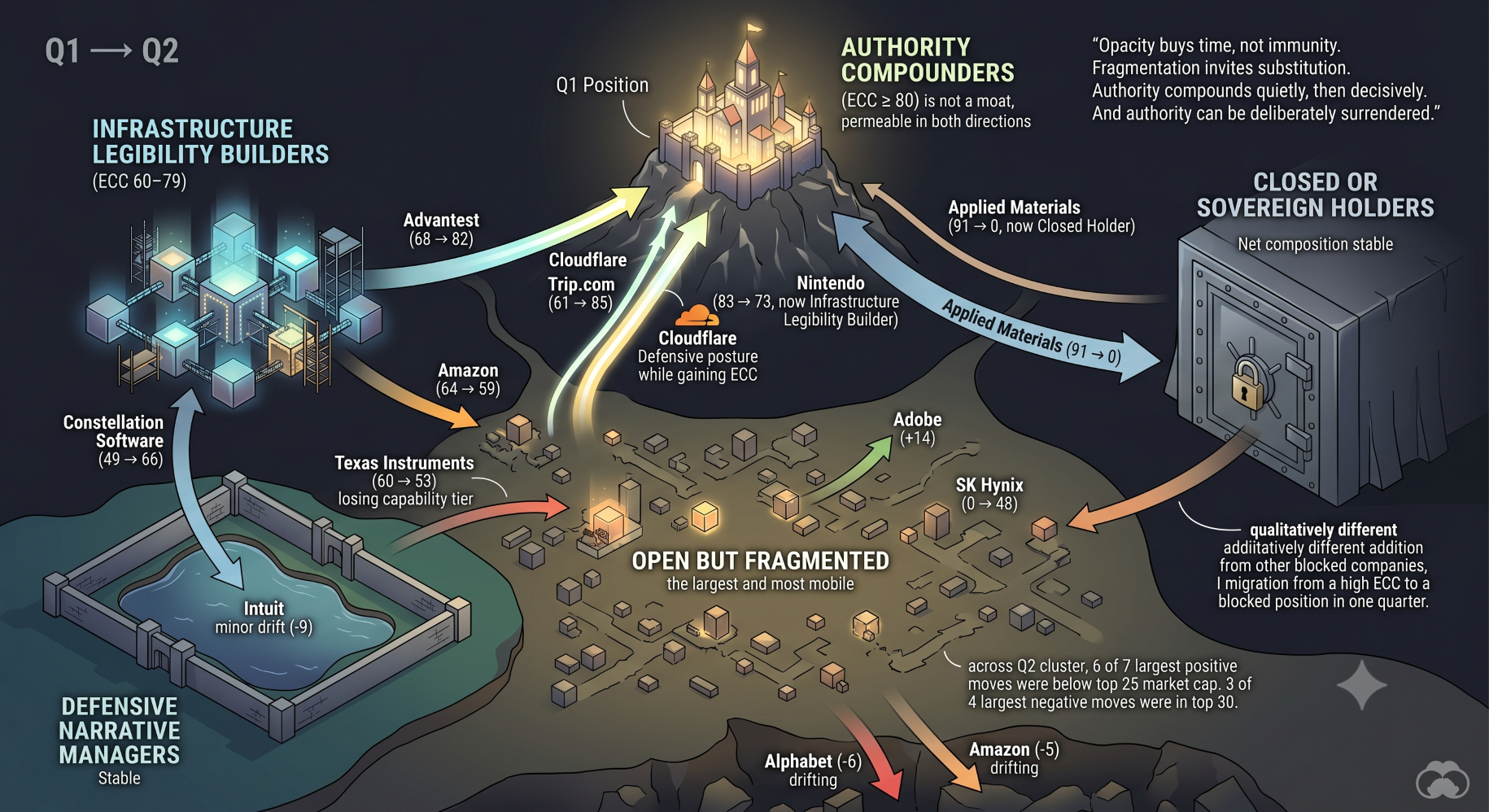

Joined in Q2: Cloudflare (68 → 84), Trip.com (61 → 85)

Exited in Q2: Applied Materials (91 → 0, now Closed Holder), Nintendo (83 → 73, now Infrastructure Legibility Builder)

Q2 confirms that Authority Compounder status is not a moat. Two companies entered. Two left. The tier is permeable in both directions.

Infrastructure Legibility Builders (ECC 60–79, non-blocked)

Gained position within tier: Advantest (68 → 82) crossed into Authority Compounder status. Constellation Software (49 → 66) crossed into this tier from Open but Fragmented.

Lost position within tier: Amazon (64 → 59) drifted into Open but Fragmented. Texas Instruments (60 → 53) lost capability tier.

Defensive Narrative Managers

Stable. No entries, no exits. Intuit drifted -9 within the tier but did not change archetype. Cloudflare entered Defensive posture while gaining ECC — a rare combined upgrade that warrants Q3 follow-up.

Open but Fragmented

The largest archetype, and the most mobile. Adobe (+14) and SK Hynix (now 48 from 0) gained ground here. Alphabet (-6) and Amazon (-5) drifted into deeper fragmentation.

Closed or Sovereign Holders

One exit (SK Hynix). One new entry (Applied Materials). Net composition stable at 21 companies.

The Applied Materials addition is qualitatively different from the existing holders. Most companies in this tier — TSMC, Tesla, Oracle, AMD, SAP, ServiceNow — have been blocked for structural or governance reasons. Applied Materials is the first company in the ECC dataset to deliberately migrate from a high-ECC Authority Compounder position into the blocked tier within one quarter.

This may indicate a new pattern: companies that previously invested in legibility are now actively withdrawing it. Q3 will indicate whether Applied Materials is alone or the leading edge.

Field 12: Strategic Implications (Rich text)

Q1 framed ECC as an authority compounding mechanism. Q2 sharpens that framing in three ways.

Authority Compounder status is not durable by default. It must be continuously maintained. Two companies left the tier in one quarter — one by choice, one by drift. Companies that achieved high ECC by accident in Q1 will lose it. Companies that achieved it through deliberate work will need to keep doing that work.

Opting out is now a documented strategy. Applied Materials moved from full legibility to full opacity in one quarter. This is the first quarter-over-quarter migration of this magnitude in any ECC dataset. It establishes a precedent: a high-ECC company can deliberately exit the AI judgment layer. The strategic question is no longer whether to be legible, but whether to remain legible once you are.

The megacap-midcap divergence is real, not anecdotal. Across the Q2 drift cluster, six of the seven largest positive moves were below the top 25 by market cap. Three of the four largest negative moves were in the top 30. If this pattern persists for two more quarters, the framework's central assertion — that ECC does not scale with market cap — will be empirically validated, not just theoretically asserted.

ECC will continue to influence capital allocation, M&A diligence framing, enterprise vendor selection, and long-term valuation narratives. Q2 adds one new use case: tracking which companies are actively withdrawing from interpretability, and at what pace.

Opacity buys time, not immunity. Fragmentation invites substitution. Authority compounds quietly, then decisively. And — Q2 adds — authority can be deliberately surrendered.

Index

Strategic Implications

Q1 framed ECC as an authority compounding mechanism. Q2 sharpens that framing in three ways.

Authority Compounder status is not durable by default. It must be continuously maintained. Two companies left the tier in one quarter — one by choice, one by drift. Companies that achieved high ECC by accident in Q1 will lose it. Companies that achieved it through deliberate work will need to keep doing that work.

Opting out is now a documented strategy. Applied Materials moved from full legibility to full opacity in one quarter. This is the first quarter-over-quarter migration of this magnitude in any ECC dataset. It establishes a precedent: a high-ECC company can deliberately exit the AI judgment layer. The strategic question is no longer whether to be legible, but whether to remain legible once you are.

The megacap-midcap divergence is real, not anecdotal. Across the Q2 drift cluster, six of the seven largest positive moves were below the top 25 by market cap. Three of the four largest negative moves were in the top 30. If this pattern persists for two more quarters, the framework's central assertion — that ECC does not scale with market cap — will be empirically validated, not just theoretically asserted.

ECC will continue to influence capital allocation, M&A diligence framing, enterprise vendor selection, and long-term valuation narratives. Q2 adds one new use case: tracking which companies are actively withdrawing from interpretability, and at what pace.

Opacity buys time, not immunity. Fragmentation invites substitution. Authority compounds quietly, then decisively. And — Q2 adds — authority can be deliberately surrendered.

Full Report

Technology's AI posture is not ideological. It is economic.

One quarter after the Q1 baseline, the framework has its first quarterly reading. Seventeen of 100 companies moved. The methodology held. The archetype structure held. What changed was the composition inside the archetypes — and one structural exit from the Authority Compounder tier.

The Applied Materials exit is the largest single signal of Q2. A company that ranked second in the Q1 index for ECC chose, in one quarter, to stop being read. This is not a capability decline. It is a deliberate decision about the cost of interpretation. The framework records a 0 because the methodology has nothing to score when a company blocks AI access — but the underlying judgment is what matters. Applied Materials decided that being legible to AI systems was no longer worth what it cost.

The Cloudflare entry is the inverse story. Cloudflare moved from Open/Medium to Defensive/High and crossed into Authority Compounder status with an ECC of 84. A combined posture-and-capability upgrade in a single quarter is rare. The Q3 question is whether Cloudflare can sustain Defensive posture while continuing to compound authority, or whether — as the Q1 thesis predicted — Defensive posture eventually compresses capability.

The Trip.com entry is the third notable structural move. The largest pure ECC gain in the dataset (+24) suggests deliberate documentation work, not accidental movement. Trip.com is now the third Asian Authority Compounder in the index, alongside Nintendo's exit and SK Hynix's unblock — a small but coherent geographic signal.

The drift cluster confirms the megacap-midcap pattern from Q1. Alphabet, Amazon, and Intel all lost ECC. Adobe, Advantest, Constellation Software, Robinhood, Schneider Electric, Keyence, and Datadog all gained. The middle of the index is doing the legibility work that the top is not.

The consolidation cluster — 83 companies that did not move — is the silent confirmation that the methodology is detecting position rather than noise. The framework is not designed to capture quarterly volatility. It is designed to capture posture and capability, both of which evolve slowly. Stability in the consolidation cluster validates this design.

Three questions will frame the Q3 reading:

- Does Applied Materials recover, partially recover, or stay at 0? The answer determines whether Q2 was an event or a structural shift.

- Does megacap drift continue? If Alphabet, Amazon, and Intel all drift down again, the "size protects authority" assumption is empirically falsified.

- Does the Asian mid-cap cluster keep moving? Three positive moves in one quarter is small but coherent. Q3 will indicate whether this is a cohort signal or a coincidence.

Authority Compounders are becoming the grammar of AI-mediated judgment. Defensive Managers are buying time. Fragmented entities are leaking narrative control. Closed holders are opting out of authority compounding entirely.

Q2 adds one new line to that frame: some companies, having achieved authority compounding, are now choosing to surrender it. Whether that becomes a pattern or remains an exception is the most important question for Q3.