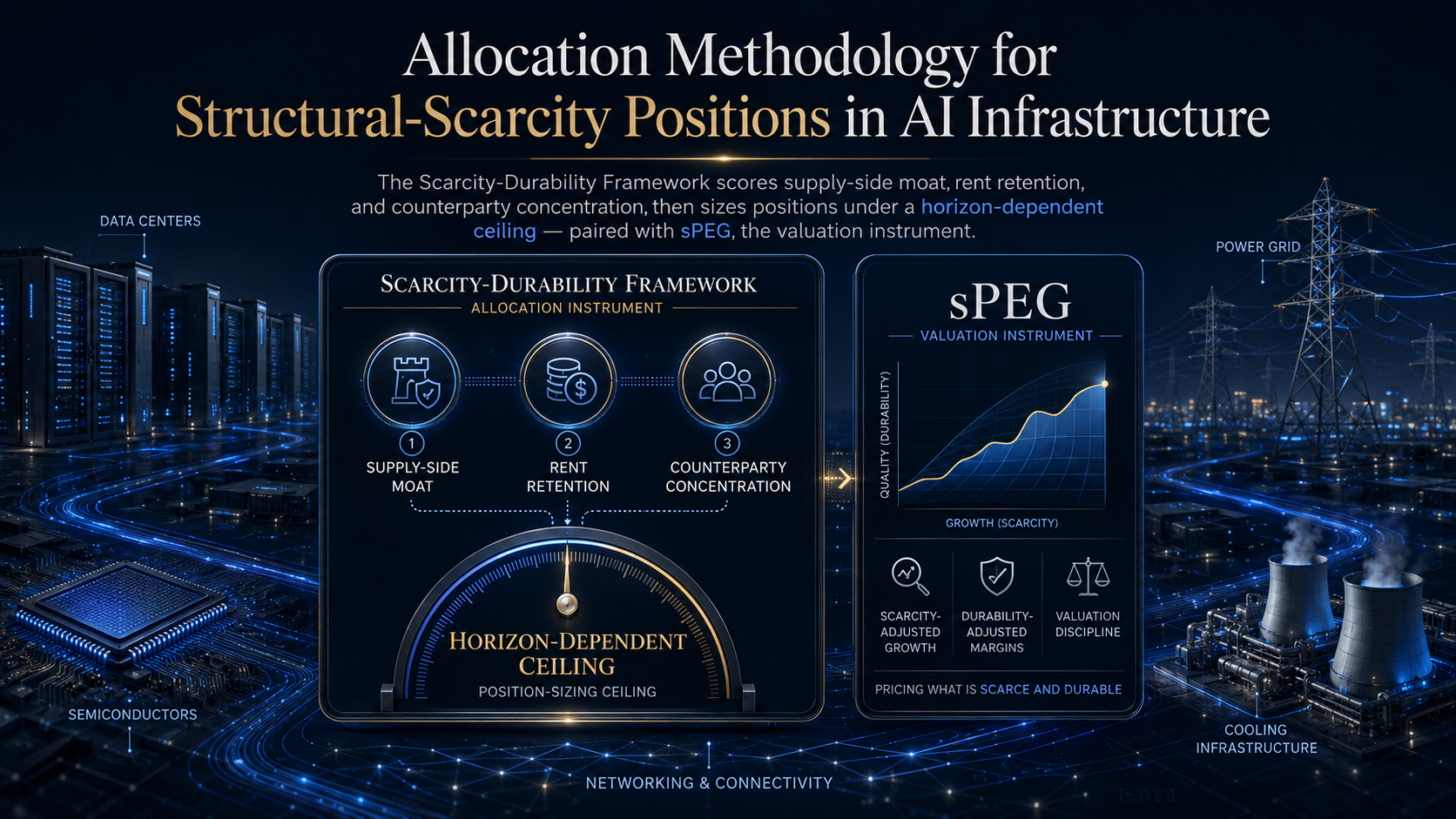

Scarcity-Durability Framework (SDF)

The allocation methodology for structural-scarcity positions in AI infrastructure. The Scarcity-Durability Framework holds that scarcity and durability are distinct: it scores an asset on supply-side moat, rent retention, and counterparty concentration, then sizes positions under a horizon-dependent ceiling. The allocation instrument paired with sPEG, the valuation instrument.

The Distinction

The Scarcity-Durability Framework begins from a claim most scarcity investing ignores: scarcity and durability are not the same thing. A real shortage can produce real pricing power that does not survive the cycle, because the same scarcity that creates the rent attracts the capacity that destroys it. Scarcity is a state; durability is a property of that state over time. Pricing the first without testing the second is how structurally sound theses become cyclical traps.

Memory is the canonical case. The scarcity is real, the pricing power is real — and it has never once been durable across a full cycle, because supply self-corrects every time. A framework that scored memory on scarcity alone would size into it at exactly the wrong point. SDF exists to separate the shortage from its durability before any capital is committed.

Position in the Stack

SDF is the allocation instrument within Applied Capital Architecture. It is one of three layers governing a structural-scarcity position:

- sPEG values the asset — what a structurally scarce name is worth.

- SDF allocates against it — whether that scarcity is durable enough, and the rent retainable enough, to size into, and how much.

- The AI Infrastructure Convergence Framework times the exit — when convergence across independent signals says the structural cycle is turning.

sPEG prices the scarcity; SDF sizes the entry; convergence times the exit. SDF is not a valuation model and not a timing system — it is the position-sizing discipline between them.

The Three Axes

SDF scores an asset on three structurally distinct questions, chosen so that strength on one is never assumed to confer strength on the others.

Supply-Side Moat. Is the advantage structural, or a temporary supply lag? A structural moat takes years and tens of billions to replicate — leading-edge fabrication, large-scale generation. A supply lag is a shortage that capacity will close. The two are nearly indistinguishable for two to three years, then diverge sharply. Scarcity that self-corrects is priced but not durable, and must be sized as such.

Rent Retention. Even where the moat holds, is the owner permitted to keep the surplus? A regulator, a ratepayer base, or a dominant counterparty may be structurally entitled to claw the rent back. Moat depth and rent capture are different questions, and they diverge most exactly where conviction runs highest — the asset that is hardest to replicate is often the one whose surplus is most contested. A deep moat with a capped ability to retain rent is a weaker position than its scarcity implies.

Counterparty Concentration. Is demand exogenous and diversified, or anchored to a small number of large, renegotiable commitments? Concentrated anchor-tenant exposure is the fastest and least-monitorable break in the entire structure — a single renegotiation can re-rate a position before any slower signal registers. For that reason it is applied not as one input among three but as a hard haircut on size, regardless of how strong the moat and rent profile appear. The discipline sizes to survive a break, not to predict or dodge it.

The Sizing Rule

The three axes resolve into a horizon-dependent position-size ceiling. On a multi-year hold, durability dominates: only structural moats with retainable rent earn meaningful size, and a supply lag is capped no matter how acute the current shortage. On a shorter trade window, scarcity and liquidity dominate the sizing and the moat requirement relaxes — but the counterparty haircut is a hard override in both horizons, because survival is not horizon-dependent.

The output is a ceiling, not a target. It defines the maximum a position may occupy given its durability and counterparty profile; it never instructs that the maximum be filled.

Standing

SDF is an allocation and position-sizing methodology — a structural reference layer for capital allocation. It is not an investment product, a performance claim, a recommendation, or a solicitation. It sits one layer above the scarcity-adjusted valuation framework and the indices it allocates against, and is operated within the governed human–AI continuum of Applied Capital Architecture, where human judgment retains decision authority.